ZTRADER PRIMER 02 |Interest Rates Are Not One Number

They Are the Price Architecture of Time, Funding, and Risk

Most market commentary treats interest rates as if the financial system contains one large dial.

Rates rise.

Rates fall.

The Fed cuts.

Bond yields move.

Markets react.

Useful shorthand. Bad mental model.

There is no single interest rate.

There is an architecture of rates, each pricing a different part of the system:

The cost of overnight money

The expected path of monetary policy

The return required to lend across time

Compensation for inflation and duration risk

The premium charged for credit and liquidity risk

The final borrowing cost faced by households and companies

A central bank can cut its policy rate while mortgage rates remain elevated.

Inflation can fall while long-term government yields rise.

Nominal yields can remain stable while real yields increase.

Treasury yields can decline while corporate financing conditions tighten.

None of these outcomes is contradictory.

They occur because “interest rates” are not one price.

They are a stack.

The One-Sentence Answer

Interest rates are a system of prices that determines how capital is transferred across time, balance sheets, and risk.

The weak question is:

Are rates going up or down?

The stronger questions are:

Which rate moved?

Which component moved?

Why did it move?

Which balance sheet must react?

Direction matters.

Composition matters more.

01 | The Price of Time

An interest rate is commonly described as the cost of borrowing money.

That is correct, but incomplete.

An interest rate is also the price of exchanging resources across time.

A borrower receives purchasing power today and promises repayment later.

A lender gives up liquidity today and demands compensation for waiting, uncertainty, and risk.

Depending on the instrument, that compensation may include:

TIME VALUE

+ EXPECTED INFLATION

+ DURATION RISK

+ CREDIT RISK

+ LIQUIDITY RISK

+ OPTIONALITY

These components do not appear in equal proportions across every market.

An overnight secured rate mainly reflects immediate funding and collateral conditions.

A long-term government yield reflects the expected path of future short-term rates plus compensation for holding duration risk.

A corporate yield adds compensation for default, downgrade, liquidity, and other risks.

A mortgage rate may also incorporate prepayment optionality, funding costs, servicing expenses, and lender margins.

The rate paid by the final borrower is therefore not simply “the central-bank rate plus a little extra.”

It is the output of several interconnected markets.

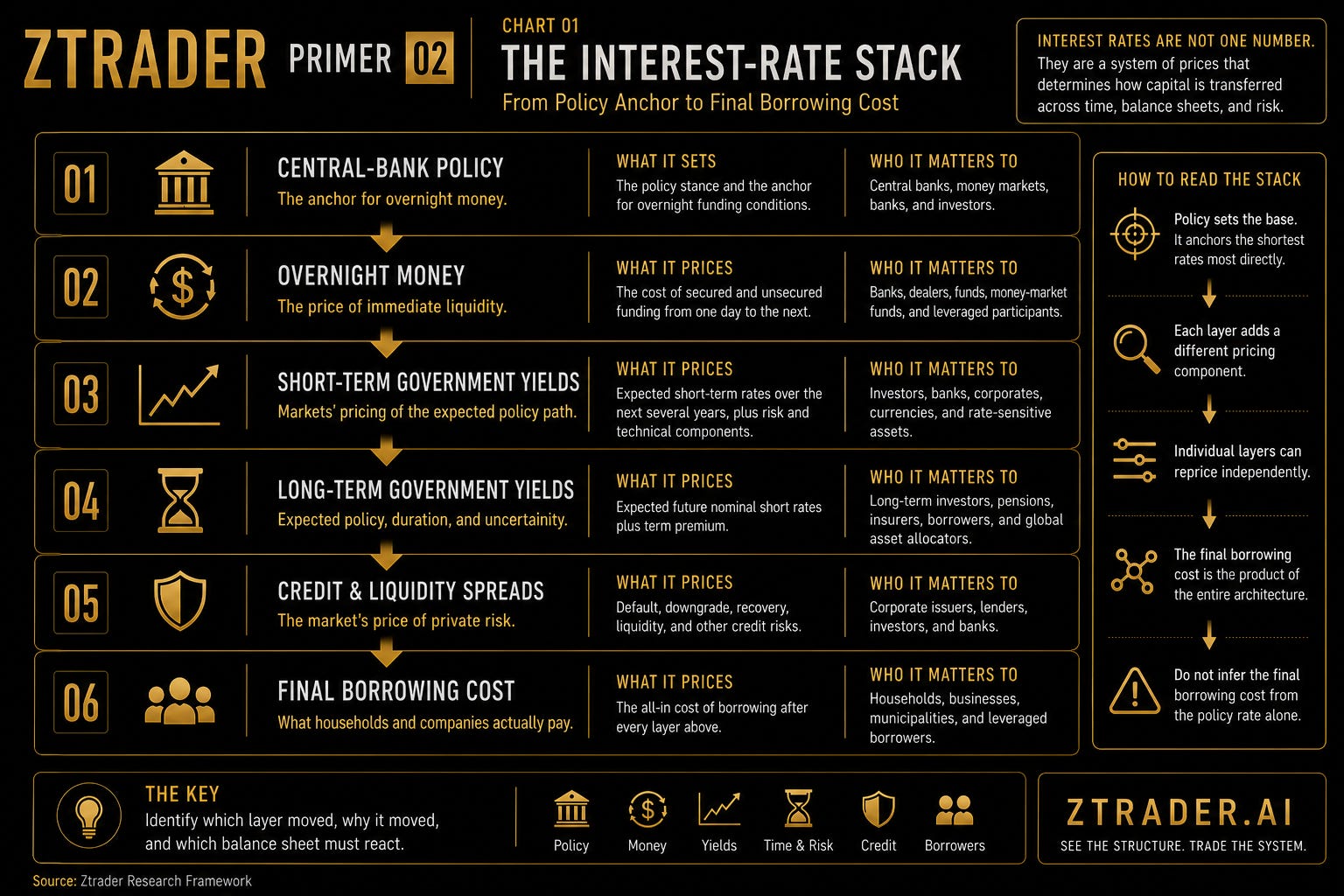

02 | The Interest-Rate Stack

For practical analysis, the rate system can be organized into six layers:

CENTRAL-BANK POLICY

↓

OVERNIGHT MONEY

↓

SHORT-TERM GOVERNMENT YIELDS

↓

LONG-TERM GOVERNMENT YIELDS

↓

CREDIT AND LIQUIDITY SPREADS

↓

FINAL BORROWING COST

This is an analytical map, not a mechanical timetable.

Markets anticipate policy before central banks act.

Credit spreads can move independently of government yields.

Long-term yields can rise because of term premium, fiscal supply, or inflation uncertainty even when the expected policy path is declining.

The stack tells us where to look.

It does not promise that every layer will move in the same direction.

Layer One: Central-Bank Policy

In the United States, the Federal Reserve establishes a target range for the federal funds rate and uses administered rates and liquidity facilities to keep overnight market rates near that range.

The policy rate therefore anchors short-term money-market conditions, but it does not directly set every yield in the financial system.

Policy affects markets through more than the current overnight rate.

It also changes:

Expectations for future rates

The cost and attractiveness of leverage

Deposit and money-market yields

Currency-rate differentials

Lending standards

Discount rates

Risk appetite

The policy rate is the anchor.

It is not the entire ship.

Layer Two: Overnight Money

Overnight rates reveal the immediate price of liquidity.

This layer includes secured and unsecured funding markets, such as repo and interbank lending.

It matters directly to:

Banks

Dealers

Hedge funds

Money-market funds

Derivatives users

Leveraged relative-value strategies

When overnight markets function normally, policy transmission tends to begin cleanly.

When repo rates, funding spreads, or collateral haircuts become unstable, the same policy stance can produce much tighter conditions for leveraged participants.

This is where monetary policy becomes an actual financing cost rather than a press-conference sentence.

Layer Three: Short-Term Government Yields

Short-term government yields are heavily influenced by the expected path of monetary policy.

The two-year Treasury yield, for example, tends to respond strongly when inflation, employment, growth, or central-bank communication changes expectations for future policy.

But the two-year yield is not a pure forecast of the policy rate.

It can also contain:

Term premium

Liquidity effects

Positioning

Hedging demand

Risk aversion

A short-term yield can fall before the central bank cuts.

It can rise while the current policy rate remains unchanged.

The front end is best understood as market pricing of the expected policy path, plus risk and technical components.

Layer Four: Long-Term Government Yields

Long-term nominal government yields can be represented as:

LONG-TERM NOMINAL YIELD

≈ EXPECTED AVERAGE FUTURE NOMINAL SHORT RATES

+ TERM PREMIUM

The term premium is the additional compensation investors require for bearing the risk of holding a long-duration security rather than repeatedly investing at short maturities.

New York Fed research explicitly decomposes Treasury yields into expected future short rates and term premium.

This distinction is essential.

Long-term yields can rise because markets expect higher future policy rates.

They can also rise because investors demand more compensation for:

Inflation uncertainty

Fiscal supply

Duration exposure

Central-bank credibility risk

Market volatility

Reduced demand for long bonds

A central bank can therefore cut its policy rate while the long end rises.

The long end is not necessarily fighting the central bank.

It may be pricing a different risk.

Layer Five: Credit and Liquidity Spreads

Government yields are only the base rate for private borrowers.

A simplified corporate borrowing yield is:

CORPORATE YIELD

≈ COMPARABLE GOVERNMENT YIELD

+ CREDIT AND LIQUIDITY SPREAD

The spread may compensate investors for:

Default probability

Recovery uncertainty

Downgrade risk

Liquidity risk

Market risk

Embedded options

Balance-sheet stress

This means that falling Treasury yields do not guarantee cheaper corporate funding.

During risk-off periods, government yields may decline while credit spreads widen.

In severe stress, wider spreads and deteriorating market liquidity can restrict issuance even when benchmark yields are falling.

The risk-free layer can ease while the credit layer tightens.

That is why Treasury yields alone do not describe financial conditions.

Layer Six: Final Borrowing Cost

The rate paid by a household or company may include:

REFERENCE YIELD

+ TERM OR DURATION PREMIUM

+ CREDIT SPREAD

+ LIQUIDITY PREMIUM

+ OPTIONALITY

+ CAPITAL AND OPERATING COSTS

Pass-through from monetary policy to mortgages and corporate borrowing costs is meaningful, but it varies across instruments, maturities, market structures, and policy regimes.

Federal Reserve research shows that policy-induced movements in Treasury yields can transmit strongly into corporate and mortgage borrowing costs, while the spreads layered above Treasury yields may still move independently.

This explains why a central-bank cut may not immediately produce:

Lower fixed mortgage rates

Easier small-business financing

Cheaper high-yield debt

Better access to bank credit

Monetary transmission is real.

It is neither instantaneous nor uniform.

Chart 01 | The Interest-Rate Stack

Source line: Ztrader Research framework; Federal Reserve and Federal Reserve Bank of New York.

03 | Short Rates and Long Rates Price Different Risks

The short and long ends of the curve do not carry the same information.

The front end is more sensitive to expected monetary policy.

The long end contains the expected path of nominal short rates plus term premium.

The relationship between them creates the yield curve.

A curve move has two dimensions:

DIRECTION

Did yields rise or fall?

SLOPE

Did short or long yields move more?

In bond-market terminology:

Bull means yields are falling and bond prices are rising.

Bear means yields are rising and bond prices are falling.

Steepening means the gap between long and short yields is increasing.

Flattening means that gap is decreasing.

Humanity has naturally chosen vocabulary in which a bull market can mean falling numbers. Apparently ordinary clarity was considered insufficiently financial.

Bull Steepening

Short-term yields fall more than long-term yields.

SHORT YIELD ↓↓↓

LONG YIELD ↓

CURVE STEEPENS

This often occurs when markets price policy easing.

It may reflect benign disinflation.

It may also reflect fear that the central bank will need to cut aggressively because growth is weakening.

The curve shape does not reveal the regime by itself.

Bear Steepening

Long-term yields rise more than short-term yields.

SHORT YIELD ↑

LONG YIELD ↑↑↑

CURVE STEEPENS

Possible drivers include:

Stronger long-term growth expectations

Higher inflation uncertainty

Rising term premium

Heavy government issuance

Fiscal credibility concerns

A bear steepener can tighten financial conditions even if the near-term policy path changes very little.

Bull Flattening

Long-term yields fall more than short-term yields.

SHORT YIELD ↓

LONG YIELD ↓↓↓

CURVE FLATTENS

This can occur when long-run growth or inflation expectations decline, safe-haven demand rises, or term premium compresses.

It may support duration assets.

It may also signal a darker economic outlook.

Bear Flattening

Short-term yields rise more than long-term yields.

SHORT YIELD ↑↑↑

LONG YIELD ↑

CURVE FLATTENS

This is commonly associated with tighter expected monetary policy.

The front end reprices sharply while the long end rises less because markets expect inflation or growth to weaken later.

Federal Reserve research similarly shows that shocks concentrated in short rates tend to flatten the curve when their effect declines across longer maturities.

The Curve Is a Relative Price, Not a Prophecy

The yield curve compares the price of money across maturities.

Its shape contains information about:

Policy expectations

Growth

Inflation

Term premium

Fiscal supply

Hedging demand

Risk appetite

An inversion can contain recession information.

It does not provide a countdown clock.

A curve is a market price shaped by expectations and risk premia, not a message delivered by an unusually well-dressed oracle.

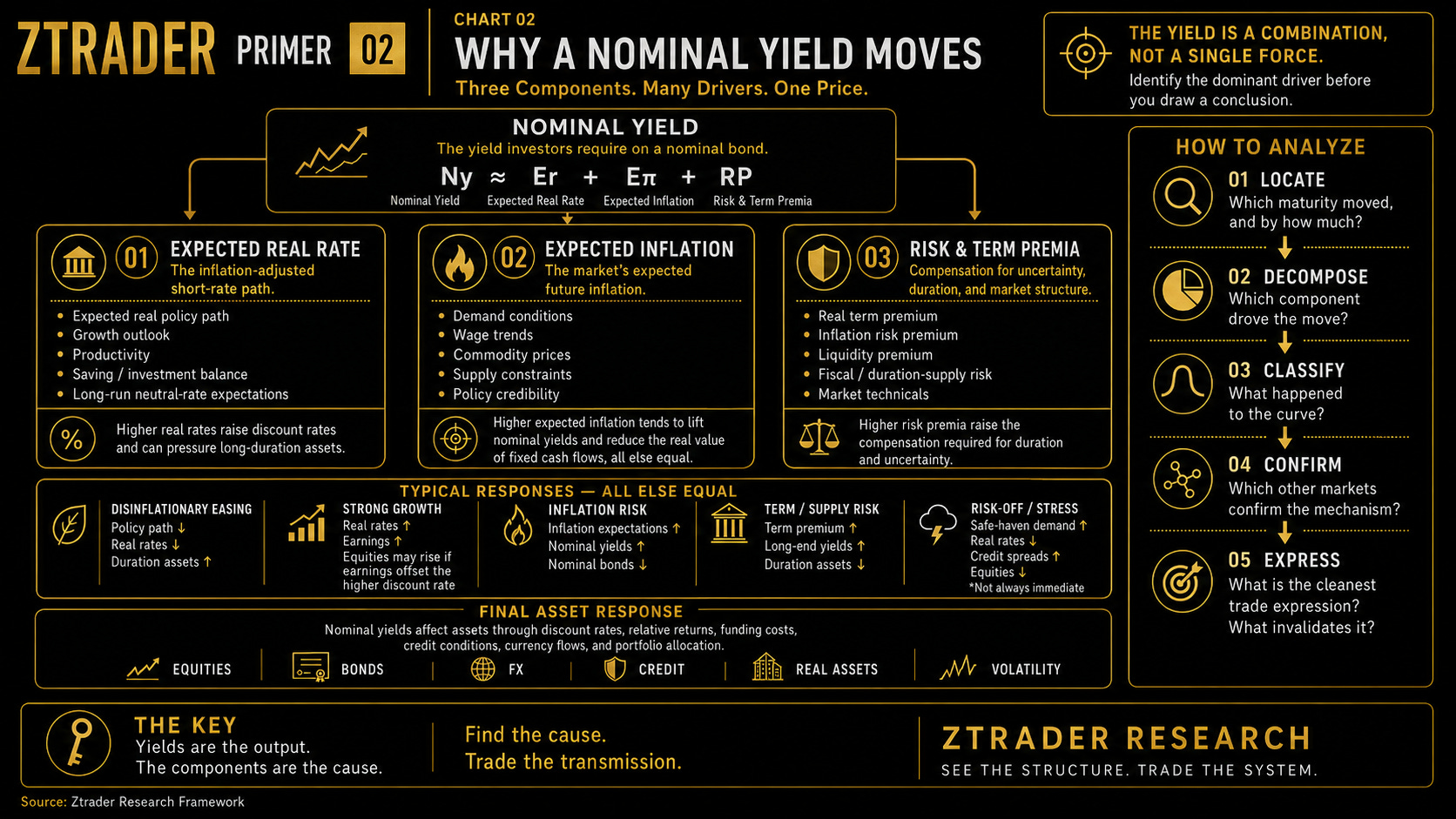

04 | Nominal Yields, Real Yields, and Inflation Compensation

A nominal government yield compensates investors in currency units.

A real yield attempts to remove the effect of inflation.

A more accurate simplified relationship is:

NOMINAL YIELD

≈ REAL YIELD

+ EXPECTED INFLATION

+ INFLATION RISK PREMIUM

Federal Reserve research notes that nominal yields include real yields, expected inflation, and inflation-risk compensation.

The difference between a nominal Treasury yield and a comparable TIPS yield is often called breakeven inflation or inflation compensation.

It is not a pure measure of expected inflation.

It can also contain:

Inflation risk premium

Liquidity differences

Market technicals

The Federal Reserve therefore describes these market measures as implied inflation compensation rather than a clean reading of expected inflation alone.

When Real Yields Rise

Higher real yields increase the inflation-adjusted return available on safer assets.

They may:

Raise discount rates

Pressure long-duration valuations

Increase the opportunity cost of holding non-yielding assets

Support the dollar through relative-return channels

Tighten external financing conditions

These are tendencies, not physical laws.

The final response depends on earnings, fiscal risk, positioning, liquidity, and the reason real yields are rising.

When Inflation Compensation Rises

Higher inflation compensation may reflect:

Stronger demand

Supply disruption

Fiscal expansion

Commodity pressure

Reduced policy credibility

Greater uncertainty about future inflation

The asset response depends on whether stronger nominal growth or higher inflation risk dominates.

Stocks may initially benefit from stronger revenues.

Margins may later weaken if costs rise faster.

Bonds may fall as investors demand more compensation.

Currencies may respond to the expected central-bank reaction rather than inflation itself.

When Nominal Yields Fall

Lower yields are not automatically bullish.

They may reflect:

Disinflation

Slower growth

Expected policy easing

Safe-haven demand

Financial stress

Falling term premium

A yield decline caused by softer inflation and stable growth may support risk assets.

A decline caused by collapsing growth expectations may occur alongside weaker equities and wider credit spreads.

“Rates down” is not a thesis.

It is an observation waiting for decomposition.

Chart 02 | Why a Nominal Yield Moves

Source line: Ztrader Research framework; Federal Reserve and Federal Reserve Bank of New York.

05 | How Rates Enter Asset Prices

Interest rates affect markets through several channels.

No channel dominates in every regime.

The Discount-Rate Channel

Asset values depend partly on expected future cash flows and the return investors require for holding them.

ASSET VALUE

≈ FUTURE CASH FLOWS

÷ REQUIRED RETURN

Higher required returns reduce the present value of distant cash flows, all else equal.

This makes long-duration assets more sensitive to real yields and risk premia.

But if yields rise because expected growth and earnings are also increasing, stronger cash flows may offset some or all of the valuation pressure.

Higher rates do not affect price in isolation.

They interact with the numerator.

The Funding Channel

Higher rates increase the cost of leverage and refinancing.

This matters to:

Property

Banks

Leveraged funds

Highly indebted companies

Private equity

Households

Governments

A business model that works with 2% financing may fail with 7% financing.

The underlying asset does not need to become less productive.

Its capital structure may simply stop working.

The Credit Channel

Monetary policy affects both the price and availability of credit.

Banks may respond to tighter conditions by raising lending rates, increasing collateral requirements, or tightening credit standards.

Central-bank research emphasizes that adjustments in lending standards form an important part of monetary-policy transmission alongside changes in market interest rates.

The quantity of available financing can matter as much as its price.

The Currency Channel

Rate differentials affect carry and international capital allocation.

Higher expected rates can support a currency.

But the result depends on:

Inflation

Growth

Fiscal credibility

External balances

Hedging costs

Risk appetite

Positioning

A high yield may represent economic strength.

It may also be compensation for instability.

Sometimes carry is income.

Sometimes it is hazard pay.

The Portfolio-Allocation Channel

Higher safe yields change the hurdle rate for every risky asset.

When investors can earn more on government securities or cash instruments, equities, credit, property, and private assets must offer greater expected compensation.

The safe rate therefore competes for capital.

It does not merely discount future cash flows.

The Expectations Channel

Markets move before central banks act.

Guidance, forecasts, economic data, and changes in the perceived reaction function can shift the expected path of rates immediately.

A central bank can tighten financial conditions without changing its current policy rate.

The market may do the tightening on its behalf, with customary enthusiasm and none of the accountability.

06 | Rate Cuts Are Not Automatically Bullish

A rate cut can occur in two very different environments.

Normalization or Insurance Cut

Inflation ↓

Growth Stable

Credit Stable

Earnings Resilient

Policy Restriction Reduced

This combination can support risk assets.

Stress or Emergency Cut

Growth ↓↓

Credit Spreads ↑

Defaults ↑

Lending Standards Tighten

Policy Reacts to Damage

This combination may arrive alongside falling equities and deteriorating credit.

The Federal Reserve lowers rates during economic downturns to support broader financial conditions, but policy easing cannot instantly remove existing credit losses, funding stress, or weak demand.

The action is the same.

The information contained in the action is not.

07 | Rising Yields Are Not Automatically Bearish

Rising yields can represent stronger growth.

They can also represent deteriorating inflation or fiscal risk.

Growth-Led Yield Rise

Growth Expectations ↑

Earnings Expectations ↑

Credit Stable

Risk Appetite Stable

Equities may absorb higher discount rates if expected cash flows improve sufficiently.

Risk-Premium-Led Yield Rise

Term Premium ↑

Inflation Risk ↑

Fiscal Concern ↑

Funding Pressure ↑

This is more likely to tighten conditions across duration-sensitive assets.

The important distinction is not simply:

Did yields rise?

It is:

Which component required investors to demand a higher return?

08 | Five Common Errors

Error One: Treating the Policy Rate as the Whole Market

The central bank most directly anchors overnight rates.

It does not mechanically set long-term yields, mortgage rates, corporate spreads, or every final borrowing cost.

Error Two: Ignoring the Component Behind the Move

A yield increase driven by stronger growth is different from one driven by term premium or inflation uncertainty.

Direction without decomposition is incomplete.

Error Three: Treating Breakevens as Pure Inflation Expectations

Breakeven inflation also contains inflation-risk and liquidity components.

It is a market price, not a laboratory reading.

Error Four: Assuming Lower Treasury Yields Mean Easier Credit

Treasury yields can fall while credit spreads widen and bank standards tighten.

The base rate and the risk spread must be read together.

Error Five: Trading Only the First-Order Effect

A rate increase may initially support a currency.

Later, tighter policy may weaken growth, damage credit, and reverse the currency move.

Rate transmission occurs in stages.

Markets inconveniently continue existing after the first candle.

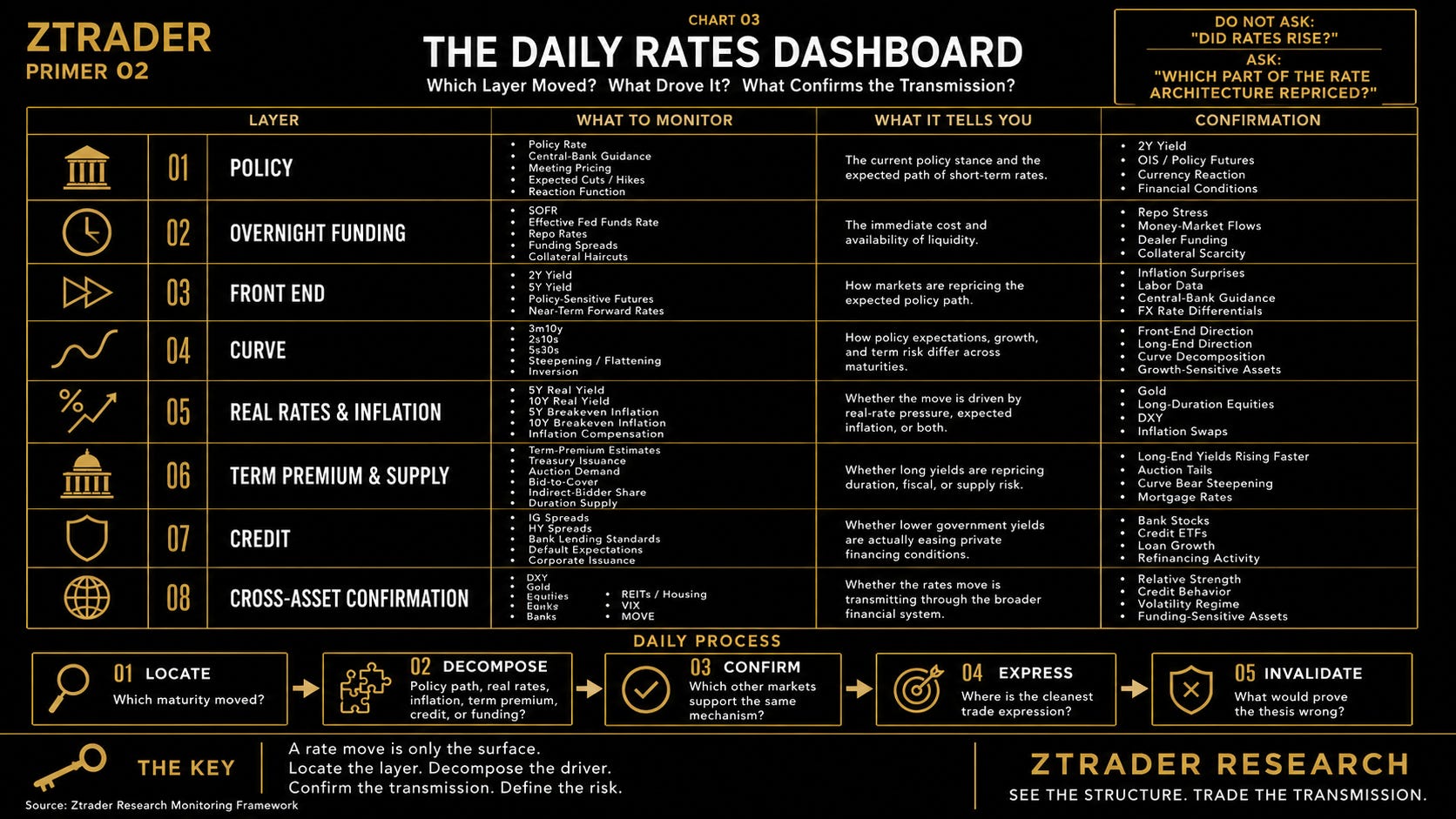

09 | How to Read Rates Each Day

Step One: Locate the Move

Which maturity changed?

Overnight

2-year

5-year

10-year

30-year

Step Two: Decompose It

Was the move driven by:

Expected policy

Real yields

Inflation compensation

Term premium

Fiscal supply

Credit stress

Market liquidity

Step Three: Classify the Curve

Was it:

Bull steepening

Bear steepening

Bull flattening

Bear flattening

Step Four: Identify the Transmission Channel

Does the move primarily affect:

Discount rates

Funding

Credit

Currency

Portfolio allocation

Bank profitability

Step Five: Demand Confirmation

Check:

DXY

Gold

Equities

Credit spreads

Banks

Property-sensitive assets

VIX

MOVE

If the other markets do not confirm the rates story, the decomposition may be wrong, the time horizons may differ, or positioning may be dominating the initial move.

Chart 03 | The Daily Rates Dashboard

01 | POLICY

Policy Rate · Central-Bank Guidance

Expected Cuts / Hikes · Meeting Pricing

02 | OVERNIGHT FUNDING

SOFR · Effective Fed Funds

Repo Stress · Funding Spreads

03 | FRONT END

2Y Yield · 5Y Yield

Expected Policy Path

04 | CURVE

2s10s · 5s30s

Steepening · Flattening · Inversion

05 | REAL RATES AND INFLATION

5Y / 10Y Real Yields

Breakevens · Inflation Compensation

06 | TERM PREMIUM AND SUPPLY

Term-Premium Estimates

Treasury Issuance · Auction Demand

07 | CREDIT

IG Spreads · HY Spreads

Bank Lending · Default Expectations

08 | CROSS-ASSET CONFIRMATION

DXY · Gold · Equities · Banks

Property · VIX · MOVE

Source line: Ztrader Research monitoring framework.

10 | From Rates View to Trade

A rates-based thesis should contain six steps:

OBSERVATION

↓

DECOMPOSITION

↓

TRANSMISSION

↓

EXPECTED CONFIRMATION

↓

INSTRUMENT

↓

INVALIDATION

Consider an example.

Observation

The 10-year yield is rising while the 2-year yield remains relatively stable.

Decomposition

The move is concentrated in the long end.

Possible drivers include:

Higher term premium

Increased duration supply

Stronger long-term growth expectations

Inflation or fiscal uncertainty

Transmission

Higher long-term yields may pressure duration-sensitive assets and increase mortgage or corporate borrowing costs.

Expected Confirmation

Look for:

Curve steepening

Higher real yields

Weakness in long-duration equities

Pressure on rate-sensitive property

Changes in Treasury-auction demand

Credit-spread behavior

Dollar confirmation

Instrument

Choose an expression with:

Direct exposure

Sufficient liquidity

Acceptable carry

Defined convexity

Clear invalidation

Invalidation

The thesis weakens if:

The long-end move reverses

Real yields fail to confirm

Auction and supply pressure recedes

Credit and duration-sensitive assets remain resilient

Evidence shows the move was growth-led rather than risk-premium-led

A rates trade is not:

Yields are rising, so short everything.

It is:

This part of the curve is repricing for this reason. These assets should respond through these channels. These observations would prove the mechanism wrong.

Primer Card 02

Interest Rates Are Not One Number

1. Which Rate Moved?

Policy, overnight, short-term, long-term, real, or credit?

2. Which Component Moved?

Expected policy, real rates, inflation compensation, term premium, or credit spread?

3. What Happened to the Curve?

Bull or bear?

Steepening or flattening?

4. Which Channel Matters?

Discount rate, funding, credit, currency, or allocation?

5. Which Balance Sheet Is Exposed?

Banks, households, companies, funds, property, or governments?

6. Which Assets Should Confirm It?

Dollar, gold, equities, credit, banks, property, or volatility?

7. What Invalidates the Thesis?

Which yield, spread, or cross-asset signal would prove the mechanism wrong?

Final Takeaway

Interest rates are not one number. They are the pricing architecture of the financial system.

The policy rate anchors overnight money.

The front end prices expected central-bank behavior.

The long end prices expected future short rates and term premium.

Real yields reveal the inflation-adjusted return demanded by investors.

Credit spreads price the vulnerability and liquidity of private balance sheets.

The final borrowing rate determines what households and companies can actually finance.

When rates move, do not stop at direction.

Locate the maturity.

Decompose the component.

Classify the curve.

Trace the transmission.

Demand confirmation.

The market does not trade “rates.”

It trades which rate changed, why it changed, and which balance sheet must react next.

ZTRADER PRIMER 02

Interest Rates Are Not One Number

The Price Architecture of Time, Funding, and Risk.

ZTRADER.AI

SEE THE STRUCTURE