The Macro PRIMER 01 Financial Market Is a System

Price Is the Last Layer You See

Markets are not a collection of isolated assets. They are a network of funding, balance sheets, collateral, expectations, positioning, and risk transfer.

Most people first encounter financial markets as a screen filled with separate prices.

Stocks rise because companies are doing well.

Bonds fall because interest rates are rising.

Gold rallies because investors are afraid.

The dollar strengthens because the US economy is strong.

Each explanation may contain part of the truth.

None is sufficient on its own.

Equities, bonds, currencies, commodities, credit, and volatility are not independent machines. They are different expressions of the same financial system.

A policy decision changes the expected path of interest rates.

That changes financing costs and discount rates.

Financing conditions alter what banks, companies, funds, dealers, and households can afford to hold.

Those balance-sheet constraints reshape positioning.

Positioning interacts with liquidity.

The result appears as price.

But the process does not stop there.

Prices change collateral values, margin requirements, volatility, and risk limits. Those changes feed back into balance sheets and generate another round of buying or selling.

The market does not simply trade news.

It trades how new information travels through the system, what has already been priced, and who is forced to react.

The One-Sentence Answer

The market is a feedback system that converts changes in policy, growth, inflation, liquidity, and risk appetite into prices, then allows those prices to reshape the system itself.

The weak question is:

Is this news bullish or bearish?

The stronger question is:

What changed, which balance sheet is affected first, what flow should follow, and where should that pressure appear in price?

The first question searches for a label.

The second searches for a mechanism.

That distinction separates market commentary from market analysis.

01 | A Five-Layer Model of the Market

The financial system cannot be reduced to one universal diagram.

It is too large, adaptive, and interconnected for that convenience.

But for practical analysis, it can be organized into five layers:

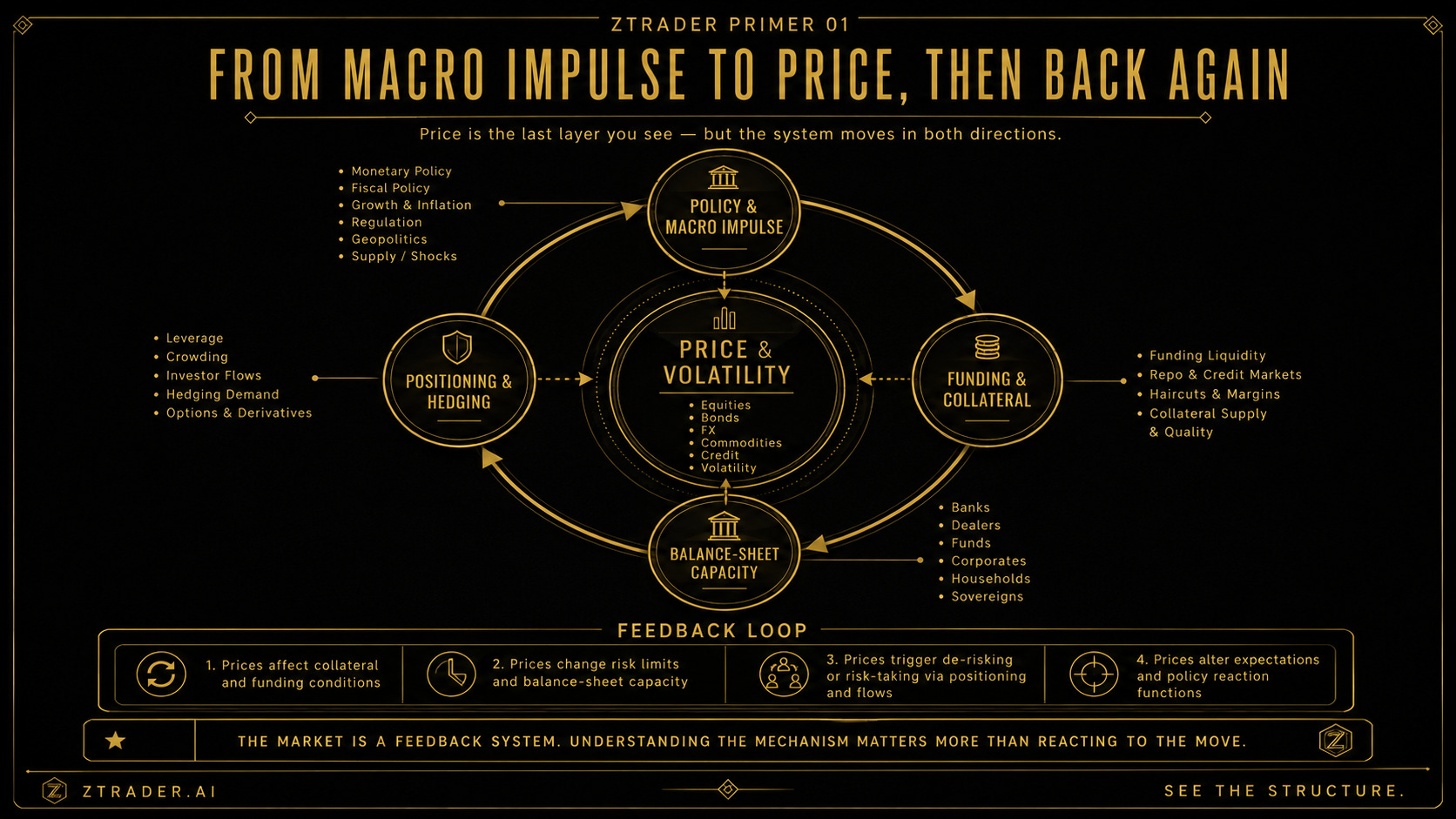

1. POLICY AND MACRO IMPULSE

2. FUNDING AND COLLATERAL

3. BALANCE-SHEET CAPACITY

4. POSITIONING AND HEDGING

5. PRICE AND VOLATILITY

This is an analytical model, not a claim that every market event follows a perfectly ordered path.

Expectations can move prices before policy is implemented.

Positioning can dominate fundamentals for a period.

A price shock can travel backward into funding and balance sheets.

The value of the model is not that it predicts every sequence. It identifies where to look for the mechanism.

Layer One: Policy and Macro Impulse

The first layer contains the information that changes the market’s expected operating environment.

It includes:

Monetary policy

Inflation

Economic growth

Fiscal policy

Government debt issuance

Regulation

Currency intervention

Geopolitical or supply shocks

Policy does not directly command assets to rise or fall.

It changes constraints, incentives, and expectations.

A central-bank rate increase can raise short-term financing costs. It may also alter the expected path of future rates, the discount rate applied to long-dated cash flows, currency differentials, lending standards, and the attractiveness of leverage.

A fiscal expansion can support growth while simultaneously increasing bond supply or inflation risk.

A decline in inflation can support bonds, unless the market is more concerned about fiscal issuance, term premium, or stronger real growth.

The market is therefore not trading a variable in isolation.

It is trading the variable relative to expectations, positioning, and the broader policy reaction function.

Layer Two: Funding and Collateral

Funding answers two questions:

Where does the money come from?

What does it cost to maintain the position?

Every financial position has a funding structure behind it.

Banks depend on deposits, reserves, and wholesale markets.

Dealers finance securities inventories.

Hedge funds use repo, derivatives, and prime-broker credit.

Companies refinance debt.

Property buyers rely on mortgages.

Governments depend on the market’s capacity to absorb issuance.

Funding liquidity is different from market liquidity.

Funding liquidity is the ability to obtain financing in a timely manner, at a predictable cost, and without excessive rollover risk.

Market liquidity is the ability to buy or sell an asset in size without moving its price excessively.

The two reinforce each other.

When financing remains available, arbitrageurs and dealers can absorb dislocations. When financing becomes unstable, otherwise manageable price gaps can become forced unwinds.

The New York Fed has emphasized this connection in the Treasury market, where stable repo funding can prevent deteriorating trading liquidity from becoming outright dysfunction.

Consider a leveraged trade dependent on cheap repo funding:

Funding Cost Rises

↓

Expected Return Shrinks

↓

Leverage Is Reduced

↓

Assets Are Sold

↓

Market Liquidity Weakens

The position may not be closed because the investor’s fundamental thesis changed.

It may be closed because the financing no longer works.

That distinction matters.

Many apparent changes in conviction are actually changes in funding capacity wearing a more respectable costume.

Layer Three: Balance-Sheet Capacity

Markets are governed by what participants can do, not only by what they believe.

Banks face capital, liquidity, and risk-weight constraints.

Dealers face inventory limits and intermediation costs.

Funds face margin requirements, redemption pressure, drawdown limits, and volatility targets.

Companies face cash-flow requirements and refinancing schedules.

Households face income, debt-service, and borrowing constraints.

These limits determine the system’s capacity to absorb risk.

Research from the New York Fed has shown that Treasury-market functionality deteriorates when dealer balance sheets are intensively used and intermediation constraints begin to bind. Liquidity can become substantially worse than yield volatility alone would suggest.

This changes how price action should be interpreted.

A fund can sell equities without becoming bearish on equities.

Losses in another position may have pushed its total portfolio risk above an internal limit.

A bank can reduce lending without making a dramatic recession forecast.

Its capital position may simply require balance-sheet contraction.

A dealer can widen bid-ask spreads without holding a directional view.

It may have insufficient capacity to warehouse additional inventory.

The useful question is not merely:

What does the market believe?

It is:

Who has the capacity to absorb this risk, and who is being forced to transfer it?

Layer Four: Positioning and Hedging

Fundamentals matter.

But prices respond to changes in fundamentals relative to expectations and existing positions.

If nearly everyone is bullish and already invested, another positive development may produce little additional buying.

If investors are deeply bearish and positioned defensively, an outcome that is merely less bad than expected can trigger a violent rally.

A useful heuristic is:

PRICE RESPONSE

≈ New Information

× Positioning Imbalance

× Available Liquidity

× Time Horizon

This is not a literal pricing equation.

It is a reminder that the same information can generate different outcomes under different market structures.

A higher-than-expected inflation print may push yields upward.

But if bond shorts are already crowded, the initial move may reverse as traders take profit, cover positions, or discover that the surprise was already embedded in pricing.

The market has not abandoned logic.

The relevant logic includes more than the economic release.

It includes expectations, convexity, hedging requirements, and the distribution of existing risk.

Layer Five: Price and Volatility

Price is where the system becomes visible.

It combines:

Expected future cash flows

Discount rates

Risk premia

Policy expectations

Liquidity conditions

Positioning

Forced transactions

Supply and demand for risk

Standard asset-pricing logic treats an asset’s value as the present value of expected future payoffs, adjusted for the return investors require to hold it. A higher discount rate can reduce that present value, while higher expected cash flows or a lower risk premium can offset the effect.

That last part matters.

Higher yields do not automatically mean lower equities.

The reason yields are rising matters.

Yields driven by stronger expected growth may coexist with higher earnings expectations.

Yields driven by inflation, policy tightening, or higher term premium may create a different cross-asset response.

Price is the final layer in the analytical chain, but not necessarily the final event in time.

Once price moves, it begins to influence the earlier layers.

Chart 01 | From Macro Impulse to Price, Then Back Again

02 | Why Different Assets Move Together

Different assets often move together because they share a common driver.

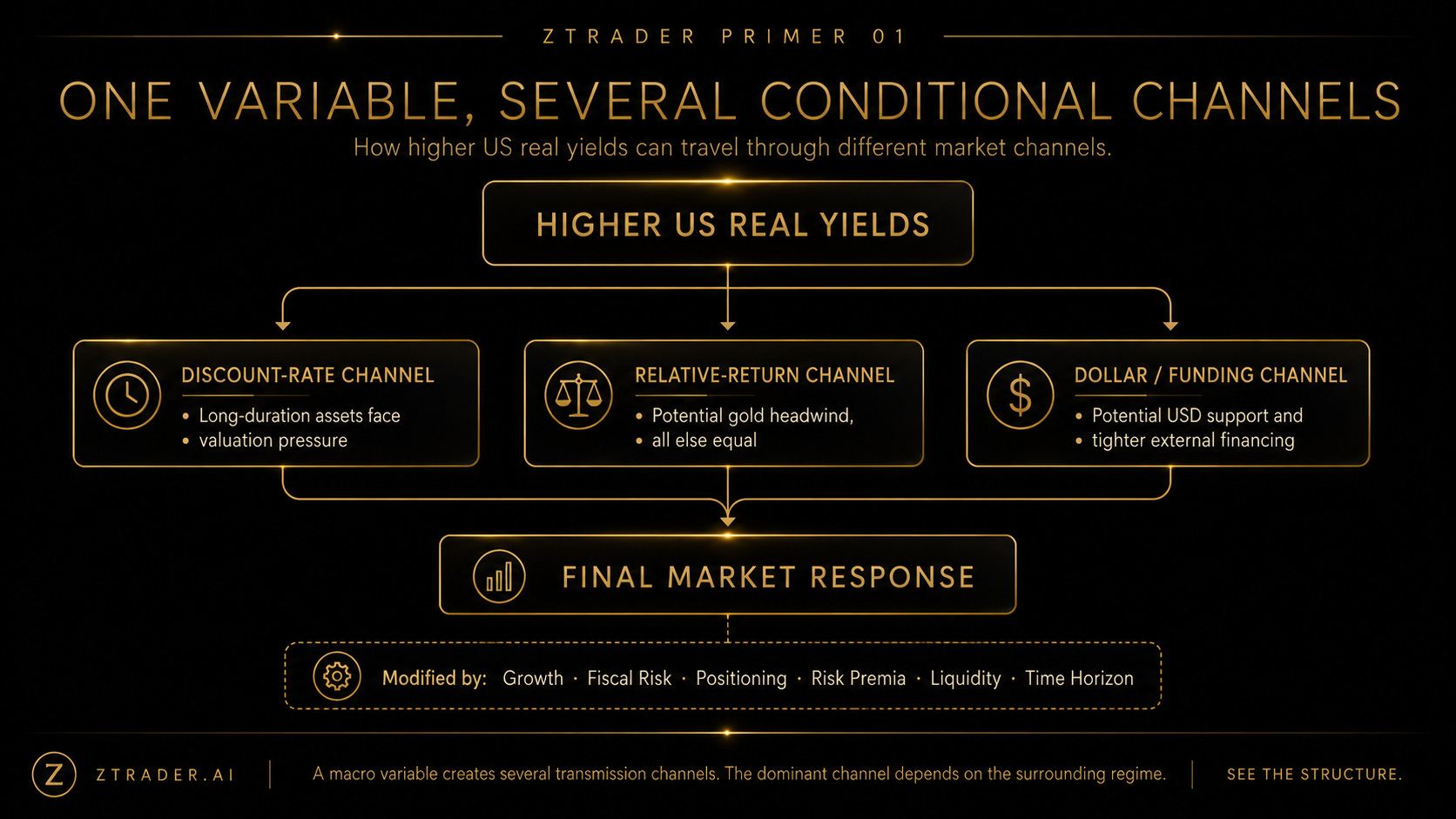

A change in US real yields, for example, may influence:

The discount rate applied to long-duration equities

The relative attractiveness of non-yielding assets

The foreign-exchange value of the dollar

Dollar-denominated borrowing conditions

Emerging-market balance sheets

Property and credit valuations

But these relationships are conditional, not mechanical.

Rising real yields can pressure long-duration valuations when expected cash flows and risk premia do not improve enough to compensate.

They can create a headwind for gold because the relative return available on interest-bearing assets has increased, all else equal. But fiscal credibility, reserve demand, geopolitical risk, inflation uncertainty, and currency confidence can overpower that channel.

The IMF similarly describes real rates as one important component of gold’s relative attractiveness rather than a complete pricing model.

Higher US yields can support the dollar, but not in every regime. The effect depends on growth differentials, policy expectations, fiscal risk, hedging demand, and positioning.

A stronger dollar can tighten conditions for economies with significant dollar liabilities because local-currency debt burdens rise and balance sheets weaken.

Federal Reserve research finds that the impact is larger where dollar-denominated credit exposure and policy vulnerabilities are greater.

The correct statement is therefore not:

Higher real yields make every risk asset fall.

It is:

Higher real yields alter discount rates, relative returns, currency incentives, and funding conditions. The final asset response depends on which channel dominates.

Chart 02 | One Variable, Several Conditional Channels

03 | The System Is Nonlinear

Market responses are not proportional to the size of the initial shock.

A ten-basis-point yield move does not carry the same meaning in every environment.

When leverage is low, liquidity is deep, and positioning is balanced, the market may absorb a substantial shock.

When leverage is high, positioning is crowded, and intermediation capacity is limited, a small trigger can cause a major repricing.

Small Trigger

+ High Leverage

+ Crowded Positioning

+ Thin Liquidity

+ Limited Dealer Capacity

= Disproportionate Price Move

The headline often explains why the move began.

The pre-existing structure explains why it became large.

This is why risk analysis should not focus only on predicting the next event.

It should identify where the system is already fragile.

04 | Feedback Loops

Financial stress can become self-reinforcing.

Price Declines

↓

Collateral Values Fall

↓

Margins or Haircuts Rise

↓

Positions Must Be Reduced

↓

Forced Selling Increases

↓

Prices Decline Further

Federal Reserve analysis has described how adverse price movements, margin calls, higher haircuts, and reduced liquidity can force leveraged institutions to sell assets and transmit stress to other participants.

The same mechanism can operate upward.

Price Rises

↓

Collateral Strengthens

↓

Measured Volatility Falls

↓

Risk Budgets Expand

↓

Leverage and Exposure Increase

↓

Price Rises Further

This explains why trends can persist beyond what a static valuation model appears to justify.

It also explains why those trends can reverse violently.

The financial system is not a passive mirror of economic fundamentals.

At times, it amplifies them.

At other times, it temporarily overwhelms them.

05 | Three Common Analytical Errors

Error One: Treating Every Asset as an Independent Story

Technology equities, gold, Bitcoin, emerging-market currencies, and high-yield credit may appear unrelated.

Yet all can be influenced by real yields, dollar funding, leverage, or risk appetite.

A single-asset explanation can mistake a system-wide shock for an asset-specific development.

Error Two: Assuming Price Reveals the Cause

A rising price may reflect stronger fundamentals.

It may also reflect:

Short covering

Passive inflows

Dealer hedging

Volatility-targeting flows

Reduced asset supply

An improvement in market liquidity

Price contains information.

It does not contain a complete explanation of itself.

Error Three: Believing a Correct Macro View Guarantees Profit

A correct economic forecast can still produce a losing trade.

You may correctly forecast slower growth but buy bonds after recession risk is already fully priced.

You may correctly forecast lower inflation but ignore fiscal issuance or rising term premium.

You may correctly expect a weaker dollar but express the trade through a currency with worse domestic fundamentals.

A trade requires more than directional accuracy.

It requires:

Thesis

+ Pricing

+ Instrument

+ Timing

+ Carry

+ Positioning

+ Risk Definition

Being right about the economy is not the same as being right about the trade.

Markets remain irritatingly unwilling to award points for intellectual effort.

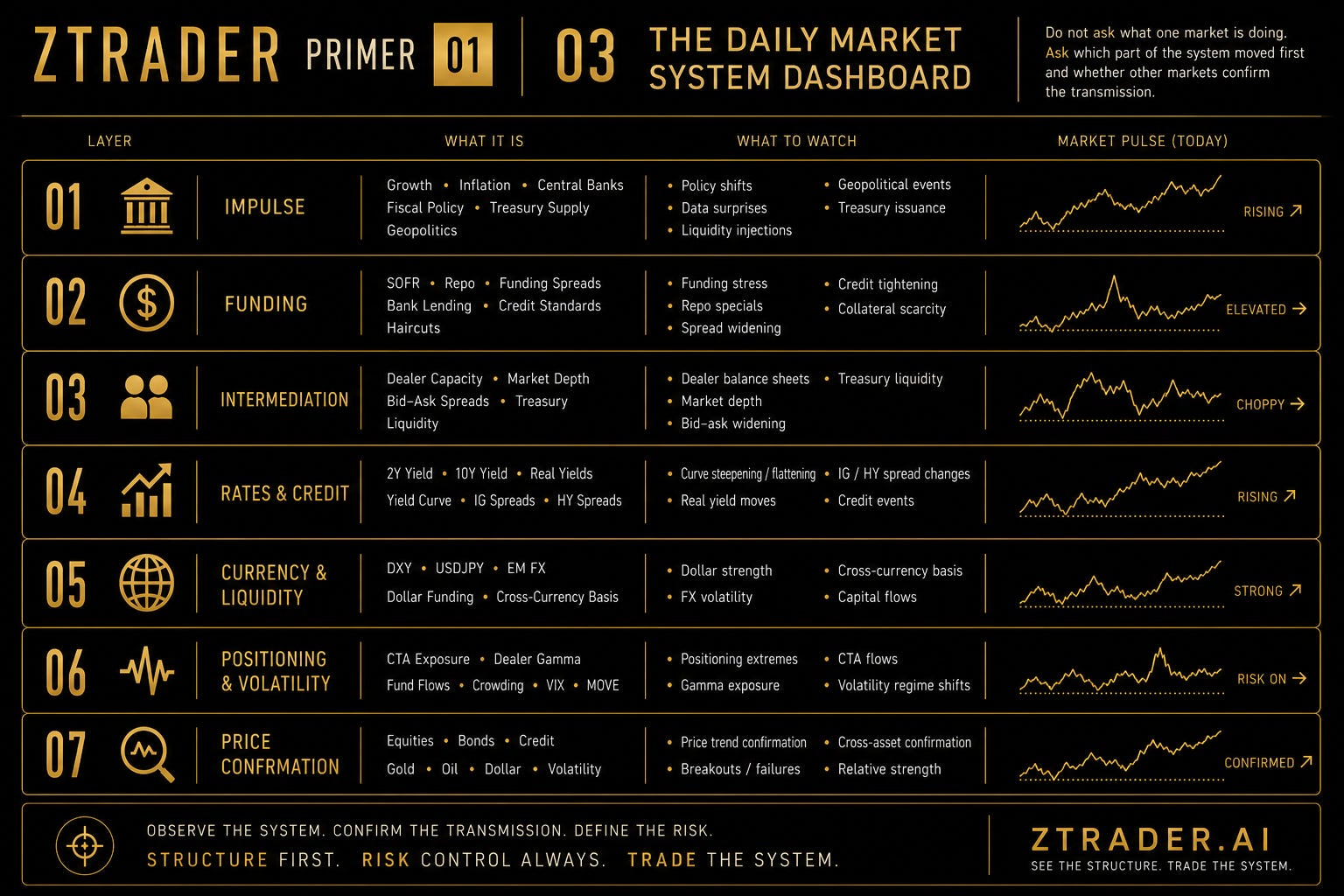

06 | How to Read the System Each Day

Do not begin with the loudest headline.

Begin with the state of the system.

1. Identify the Impulse

What changed?

Growth

Inflation

Monetary policy

Fiscal policy

Government issuance

Regulation

Supply conditions

2. Identify the First Transmission Channel

Did the change enter through:

Discount rates

Funding costs

Currency markets

Credit conditions

Expected cash flows

Risk premia

3. Locate the Vulnerable Balance Sheet

Who is most exposed?

Banks

Dealers

Leveraged funds

Corporates

Governments

Households

Emerging-market borrowers

4. Read Positioning

What was already expected?

Where is the crowd?

Who may need to hedge, cover, rebalance, or deleverage?

5. Demand Cross-Asset Confirmation

Do rates, currencies, credit, commodities, equities, and volatility tell the same story?

If not, which market is leading and which is lagging?

A divergence is not automatically an error.

It may reveal that different markets are pricing different horizons or different parts of the mechanism.

Chart 03 | The Daily Market System Dashboard

07 | From System View to Trade

System thinking is not designed to make the process more complicated.

It is designed to prevent bad attribution.

A complete trade thesis should move through six steps:

Observation

↓

Mechanism

↓

Expected Confirmation

↓

Instrument Selection

↓

Risk Definition

↓

Invalidation

Consider an example.

Observation

US real yields are rising.

Mechanism

Discount rates are increasing and dollar funding may become more restrictive.

Expected Confirmation

Long-duration equities weaken relative to the broader market.

The dollar strengthens.

Gold struggles unless fiscal, geopolitical, or reserve-demand channels dominate.

Emerging-market credit or currencies begin to show pressure.

Instrument Selection

Choose the market where:

The transmission is most direct

Liquidity is sufficient

Carry is acceptable

The move is not already fully priced

Risk Definition

Specify:

Entry

Maximum loss

Time horizon

Relevant volatility

Event exposure

Position size

Invalidation

The thesis weakens if:

Real yields reverse sustainably

The dollar fails to confirm

Credit remains resilient

Long-duration equities outperform despite the expected tightening channel

A different macro force becomes dominant

A trade should not begin with:

I think this asset will rise.

It should begin with:

This variable changed. Here is the mechanism. These markets should confirm it. This outcome would prove the thesis wrong.

That is a tradeable structure.

Primer Card 01

The Market Is a System

1. What Changed?

Was the initial impulse policy, growth, inflation, funding, fiscal supply, or risk appetite?

2. Which Channel Matters?

Discount rates, cash flows, credit, currency, collateral, or liquidity?

3. Who Is Exposed?

Which balance sheet benefits, and which becomes constrained?

4. What Was Already Priced?

Is the market surprised, or merely receiving confirmation of an existing consensus?

5. Which Assets Should Confirm the Thesis?

What should happen in rates, FX, credit, equities, commodities, and volatility?

6. Where Is the Feedback Loop?

Could price movements alter collateral, margin, volatility, or risk capacity?

7. What Invalidates the Trade?

Which observable change would prove the expected transmission is not occurring?

Final Takeaway

The market is not a screen full of prices. It is a network of constraints, expectations, and feedback loops.

Price is the visible layer.

Below it sit the cost of funding, the availability of collateral, the capacity of balance sheets, and the distribution of positions.

A market move becomes meaningful only when you understand what produced it and what it may force participants to do next.

Bonds describe the price of time and capital.

Currencies reveal relative policy and global funding pressure.

Credit exposes balance-sheet fragility.

Volatility prices the transfer of risk.

Equities express expectations for future cash flows and the rate used to discount them.

These markets are not telling unrelated stories.

They are describing different parts of the same system.

Do not begin by asking whether the next headline is bullish or bearish.

Begin by tracing the transmission.

ZTRADER PRIMER 01

The Market Is a System

Price Is the Last Layer You See.

ZTRADER.AI

SEE THE STRUCTURE