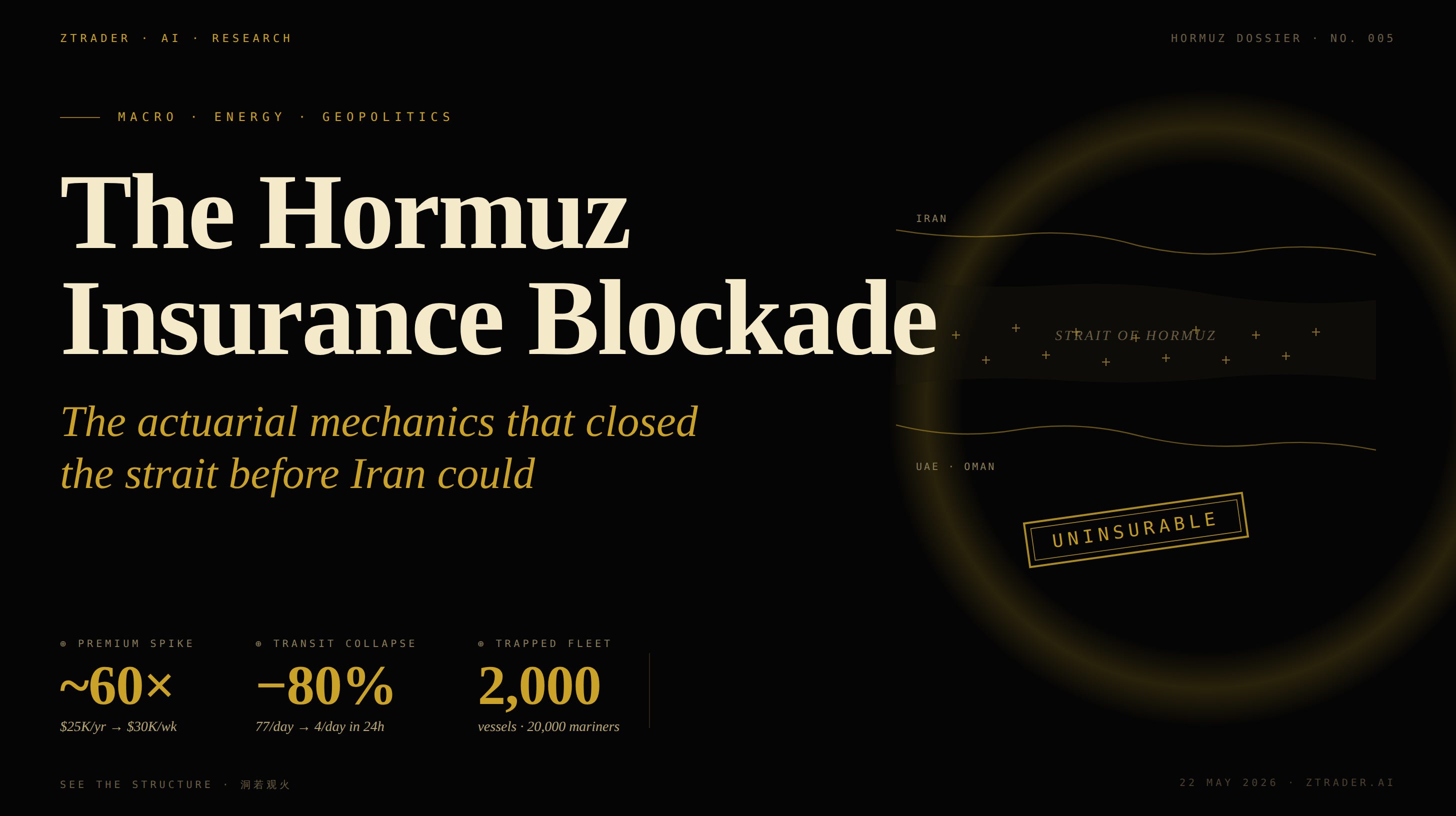

The Hormuz Insurance Blockade:How London Closed the Strait Before Iran Could

The actuarial mechanics that closed the strait before Iran could

The Strait of Hormuz did not close because the IRGC laid mines. It closed because war-risk insurance became unpriceable. Brent ran +70%, JKM ran +137%, Frontline ran +62% — and the actionable signal preceded the headlines by 72 hours, in publicly available reinsurance bulletins.

ZTrader.AI Research · Hormuz Series · 22 May 2026

I. Midnight, 5 March 2026

At midnight GMT on 5 March 2026, the Strait of Hormuz closed. Not because Iran sank a fleet. Not because the IRGC laid an impenetrable minefield. Not because U.S. naval escorts failed. The strait closed because, in that single hour, war-risk insurance policies for vessels entering the Persian Gulf were extinguished. Without that piece of paper, the global merchant fleet does not move — banks will not finance, charterers will not sign, terminals will not berth.

The mechanism was elegant. On 2 March, the International Group of P&I Clubs — a mutual risk pool that covers roughly 90 percent of the world’s ocean-going tonnage — issued 72-hour notices of cancellation to its members. All twelve clubs. Same wording. Same effective date. Gard, Skuld, NorthStandard, the London P&I Club, the American Club, Steamship Mutual. By the time the clock struck midnight three days later, more than 150 tankers were idling outside the chokepoint, waiting for coverage that no longer existed in the private market.

Iran’s Revolutionary Guards had declared the strait closed and threatened to “set on fire” any vessel attempting passage. But that threat is not what shut down the waterway. The shutdown was executed by a clause in a reinsurance contract, signed in a London office, exercised under a 72-hour notice period. Tehran provided the trigger. London pulled the lever.

“Iran’s Revolutionary Guards Navy has never sunk a vessel in the Strait of Hormuz. Markets did — with an electronic signature, not a torpedo.”

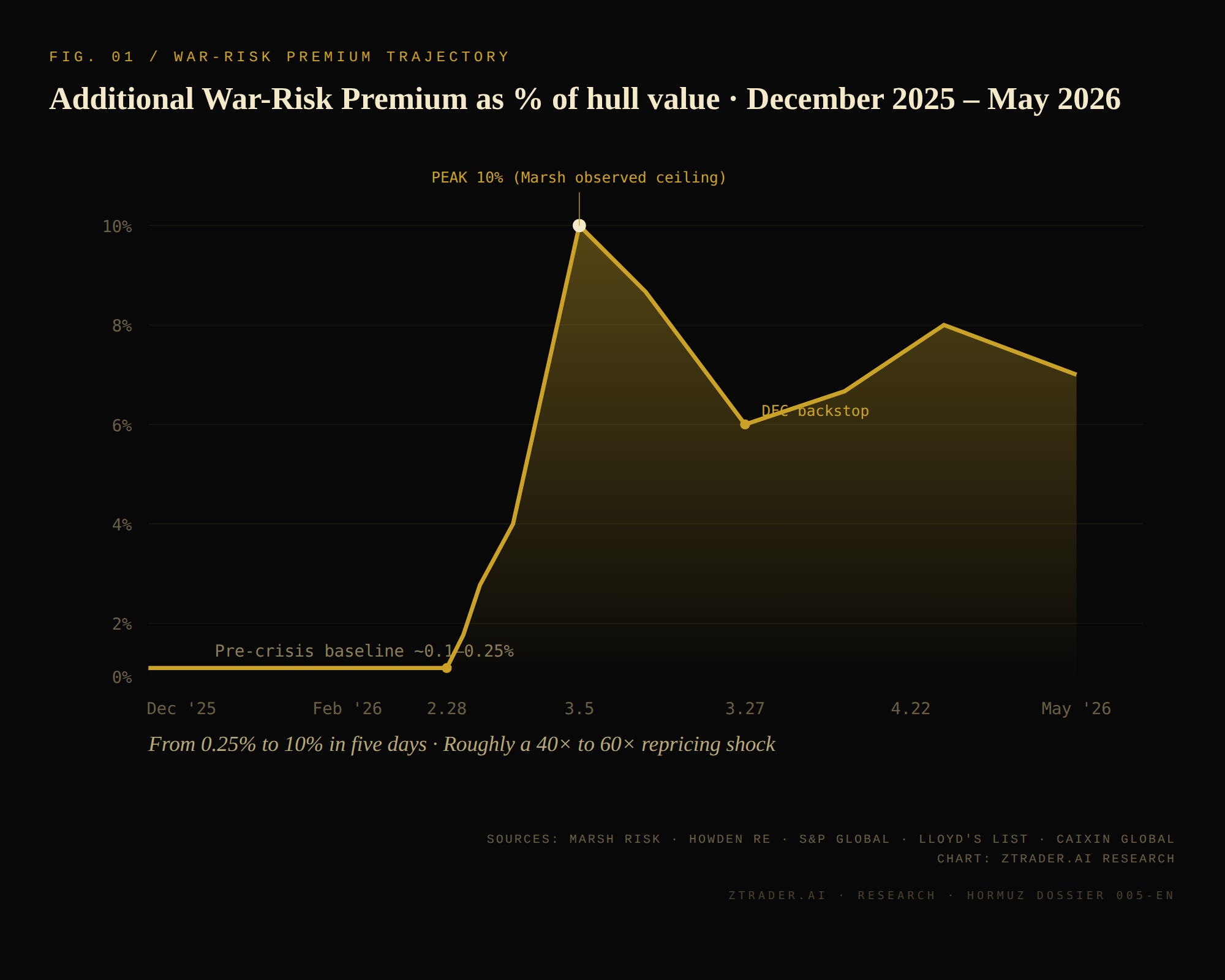

[FIG. 01 — WAR-RISK PREMIUM TRAJECTORY: from 0.25% baseline to 10% peak in five days]

II. The three-step cascade

Read only the premium chart and you miss the mechanism. What happened between 28 February and 5 March was not a price move — it was a phase transition. The shutdown ran through three self-executing steps, each triggered by the one before it. The vocabulary comes from the Irregular Warfare Initiative, but the architecture sits inside ordinary commercial contracts that have existed for decades.

Step one — Repricing. Within 48 hours of the U.S.–Israeli strikes, Additional War-Risk Premiums (AWRPs) climbed from roughly 0.15–0.25 percent of hull value to 1 percent, renewable every seven days. For a $100 million VLCC, that meant an incremental cost of roughly $800,000 per voyage. Expensive, but absorbable. Two million barrels of crude at then-prevailing spreads still cleared the math. Traffic slowed, but did not stop.

Step two — Coverage expiry and prohibitive replacement. On 2 March, reinsurers backing P&I clubs’ charterers’ liability books exercised their right to exclude Gulf claims at 72 hours’ notice. The clubs, in turn, issued Notices of Cancellation (NOCs) to their members. Here a subtle point matters: NOCs are not designed to cancel coverage outright — they are contractual mechanisms that simultaneously cancel and re-offer cover on revised terms. The terms simply became so extreme that no rational owner could accept them. Lloyd’s List later documented the magnitude: coverage that had cost approximately $25,000 per year was re-offered at $30,000 per week. A roughly 60× repricing. Coverage technically remained available. Practically, it had ceased to exist.

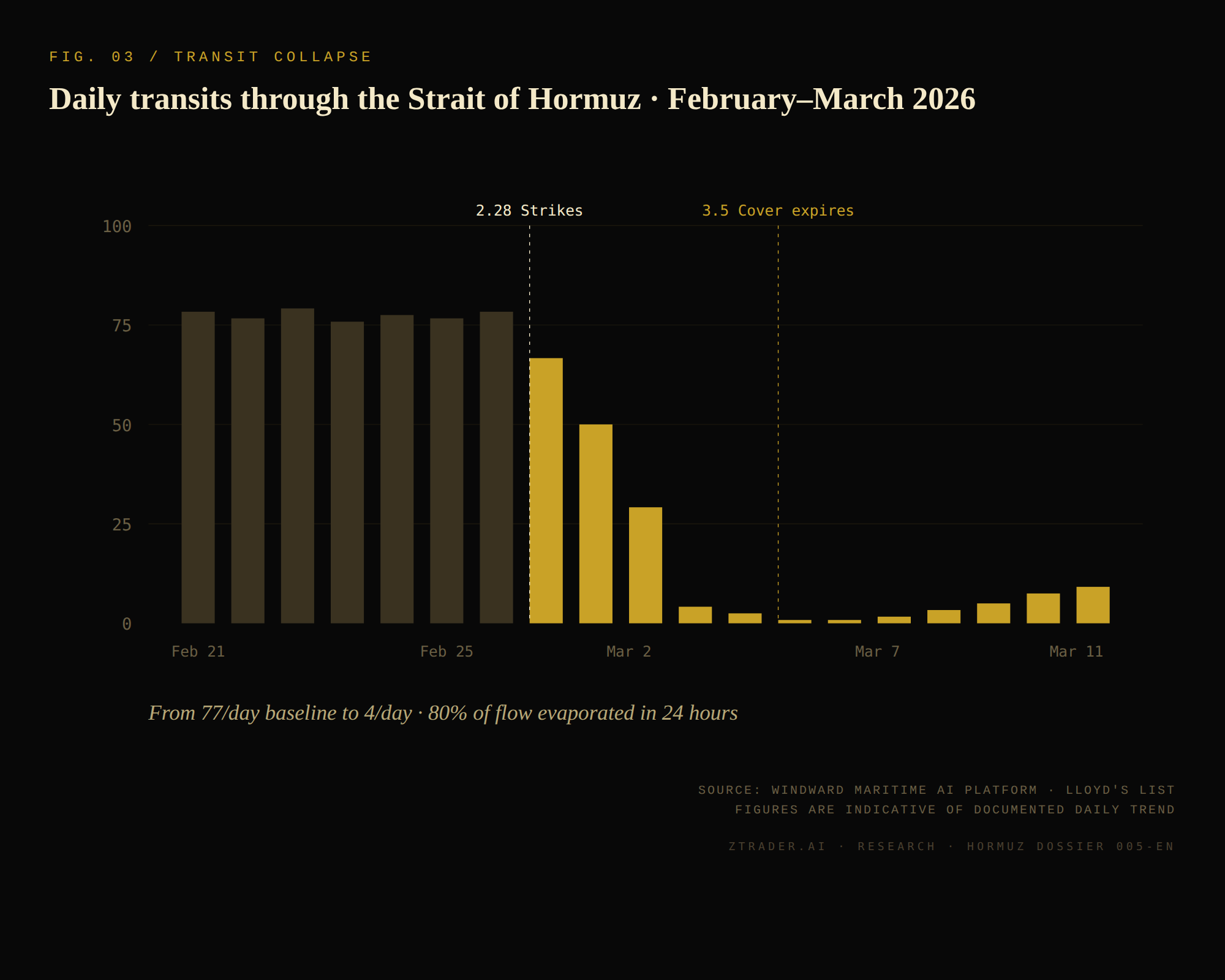

Step three — Owner self-exit. No one ordered ships to stop sailing. But a vessel without baseline P&I cover cannot call at any major port — charterers refuse to fix, terminals refuse to berth, banks refuse to finance, third-party liability becomes unbounded. By 3 March, transits had collapsed from a seven-day average of roughly 77 vessels per day to four. By 5 March, when the cancellations took effect, the strait was functionally closed. Iran had not yet fired most of the shots that followed. The strait closed itself — under the legal architecture of London marine reinsurance.

“The strait closed before the IRGC navy ever needed to act. The strait closed because reinsurers in London decided they could no longer price the risk — and once you cannot price it, you exit.” — Synthesis from Lloyd’s List, Howden Re, Small Wars Journal

⊕ Counterpoint · Lloyd’s List

It is worth registering the industry’s own pushback. “No, P&I clubs have not cancelled war-risk cover,” Lloyd’s List argued on 8 March. The clubs themselves were privately furious at being characterized as the agent of closure. Their argument: reinsurers forced the move at 72 hours’ notice — the clubs were not authors but transmitters of a decision made above them. This is technically correct. But the distinction is moot for the shipowner who finds, at midnight on 5 March, that no insurance is buyable at any price they can stomach. The institutional finger-pointing only reinforces the deeper point: no single actor closed the strait. The system closed it.

III. Timeline of the cascade

From the military strike to the maritime shutdown, the entire sequence ran in under five days.

28 Feb · D-0 — Military trigger. Coordinated U.S.–Israeli strikes on Iranian nuclear and military infrastructure. Iran announces “closure” of the strait. Markets still functioning.

1 Mar · D+1 — Step one: repricing. AWRPs jump from ~0.25% to 1%. A laden VLCC’s per-voyage premium rises from ~$625K to ~$2.5–3M. Still absorbable.

2 Mar · D+2 — Reinsurance exits. Reinsurers exercise 72-hour exclusion clauses. All twelve International Group P&I clubs issue NOCs the same day.

3 Mar · D+3 — JWLA-033 expansion. Lloyd’s Joint War Committee re-designates the entire Persian Gulf, Gulf of Oman, plus Bahraini, Kuwaiti, Omani, Qatari, and Djiboutian waters as conflict-listed. Transit volume drops from seven-day average of 77 to 4.

5 Mar · D+5 · 00:00 GMT — The actuarial blockade takes effect. 72-hour notices expire. 150+ tankers idle outside the strait. Hormuz is functionally closed.

8 Mar · D+8 — China follows. The China Shipowners’ Mutual Assurance Association adopts JWLA-033 effective midnight GMT 8 March. The exclusion is now globalized.

Early April · D+30 — Sovereign backstop. Trump administration directs U.S. International Development Finance Corporation (DFC) to establish a $40 billion revolving reinsurance facility. The DFC — created 2019 for emerging-market infrastructure — is repurposed in 72 hours as sovereign insurer of last resort.

May 2026 · D+80 — New baseline. War-risk premiums stabilize in 1%–8% range — never returning to 0.1–0.25% peacetime world. Red Sea (2024–25) + Hormuz (2026) = permanent structural repricing of marine war risk.

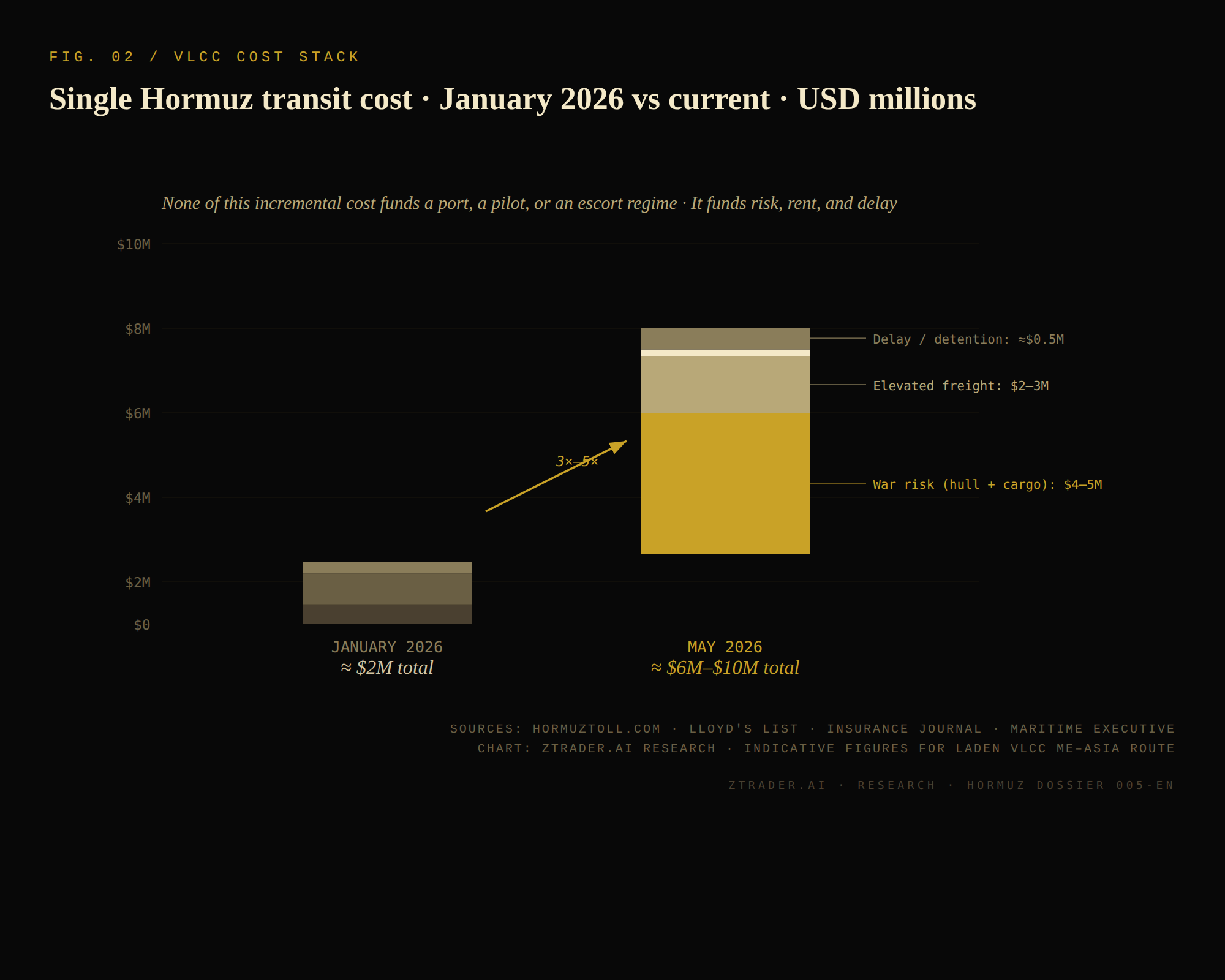

[FIG. 02 — VLCC COST STACK: ≈$2M (January 2026) → ≈$6–10M (current)]

[FIG. 03 — TRANSIT COLLAPSE: 77/day → 4/day in 24 hours, −80%]

IV. Why this is not 1987

A practitioner will note that the Tanker War (1984–88) produced its own insurance shock. Premium rates moved from approximately 0.0125 percent to 0.5 percent over the conflict cycle, before subsiding to roughly 0.0375 percent by late 1990. So what is genuinely new?

The shape of the contract is new. During the Tanker War, insurance always remained available — just more expensive. Shipowners could perform a rational calculation: a cargo of two million barrels worth roughly $250 million dwarfed even a $6 million premium. The actual hit rate on tankers was below 1 percent. Insurers could model the risk, so they could price it, so the market kept clearing.

In 2026, the buried sentence in Lloyd’s List coverage is the diagnosis: reinsurers withdrew not because they computed an unaffordably high rate, but because they could no longer compute a rational rate at all. The uncertainty around Iran’s attack patterns — drones, missiles, fast-boat swarms, mines, asymmetric proxies — broke the actuarial model. When uncertainty exceeds modelable risk, insurance flips from a continuous pricing function to a binary switch. That binary mode is the new feature.

“The question is no longer whether insurance got expensive. The question is that insurance became a switch — and the switch is in London.”

This is also why the Trump administration’s DFC backstop matters, but only to a point. A 2019-vintage emerging-market finance vehicle is being repurposed as a sovereign insurance of last resort because no domestic peacetime mechanism exists for this kind of failure. The Irregular Warfare Initiative reads it cleanly: “A sovereign guarantee improvised 72 hours into a crisis is not a strategy. It is a scramble.” The scramble worked — freight futures dipped on the DFC announcement, traffic partially resumed. But the structural exposure remains.

V. The phantom navy: how a shattered force still closes a strait

A reasonable objection presses against everything written so far.

By mid-March, Iran’s conventional naval power had been gutted. The United States and Israel struck the IRGC naval headquarters, the shipyard at Bandar Abbas, the Caspian flotilla. President Trump publicly claimed nine Iranian naval ships destroyed in the opening 48 hours; ACLED tracked U.S. strikes destroying 17 Iranian warships, including a submarine; the U.S. Navy reportedly identified and destroyed 16 to 28 fast minelaying boats within a few days as Iran attempted to seed the strait. Supreme Leader Khamenei was killed in the opening wave.

The senior IRGC, defense, and intelligence chain of command was decapitated. By any conventional metric, Iran’s ability to physically interdict the strait was severely degraded by the end of week one.

So how did the blockade persist? The U.S. intelligence battle-damage assessment released on 22 April provides the clean number: roughly 60 percent of IRGC naval assets remained operational at the time of the early-April ceasefire. Half the ballistic-missile stockpile survived. Iran’s pre-conflict design — dispersal, hardened underground facilities, decentralized command, asymmetric platforms — limited the strike campaign’s actual effect on its denial capability. The Iraqi pattern (centralized command, decapitate the top, system collapses) did not apply. Tehran had deliberately built a system that would degrade gracefully under decapitation.

Yet even 60 percent overstates what is operationally relevant for a closure. The strait does not need to be physically closed every day. It needs to be uninsurable every day. And uninsurability requires only one thing from Iran’s residual force: credible randomness. A handful of fast boats, a few dozen surviving anti-ship cruise missiles, a small inventory of mines, and a willingness to use them on an unpredictable schedule against unpredictable targets — that is the entire input the actuarial system needs to refuse a price.

“The remarkable feature of this conflict is not how much of Iran’s navy was destroyed. It is how little of it Iran needed to keep the strait closed.”

This is the asymmetry the insurance mechanism creates, and it inverts conventional military logic. In a conventional blockade, the blockading force must be strong enough to defeat the defender’s challenge. A weak blockader fails. But in an insurance-mediated blockade, the attacker need only be strong enough to make the defender’s risk unmodelable. Those are entirely different thresholds — and the second one is dramatically lower than the first.

Consider the actuarial calculus. A reinsurer setting a premium needs three inputs: expected attack frequency, expected loss given attack, and the variance around both. After 28 February, frequency became unstable (drones, missiles, mines, fast boats, all in unpredictable combination), loss-given-attack became unbounded (single VLCC loss = ~$250M hull + cargo, plus crew, plus environmental liability), and variance exploded. It is the variance that breaks the model, not the mean. A predictable threat of high magnitude can be priced. An unpredictable threat of moderate magnitude cannot. The 9–15 vessel hits that actually occurred between 28 February and end of March were not numerically catastrophic — but they were temporally and geographically scattered enough that no actuarial extrapolation held.

This produces what defense economists call a force-multiplier ratio that has no equivalent in pre-financial-infrastructure warfare. In 1987 — even at the peak of the Tanker War — the U.S.-flagged tanker reflagging program (Operation Earnest Will) physically escorted convoys, and the actual hit rate stayed below 1 percent. Iran needed substantial naval forces to maintain a roughly 1 percent attrition rate. In 2026, Iran achieved an 80 percent traffic collapse with a residual fraction of its 1987-equivalent force, because the closure was not executed by Iranian boats — it was executed by the absence of a reinsurance signature in London. Iran provided the uncertainty input. The market converted that input into a closure output. The leverage ratio between Iranian kinetic effort and resulting trade disruption may be the highest in the history of naval warfare.

There is a darker reading. If a 60-percent-degraded navy plus credible asymmetric residuals is sufficient to close the world’s most critical energy chokepoint via the insurance channel, then every chokepoint defender in the world has just been handed a manual. The Houthi precedent in the Red Sea (2023–25) was the first proof of concept. Hormuz (2026) is the validation at scale. The next iteration will not require destroying anyone’s navy first — it will require only the credible suggestion that a navy might act unpredictably. That suggestion is now a sufficient instrument of blockade.

The entire structure is interesting.

BUT The trade is what pays.

What follows is a per-asset post-mortem of the Hormuz shock

— Brent peaks, the Brent–WTI spread as a listed insurance contract, JKM’s

+137% move and the JCC transmission window, Frontline’s path from

$21 to $37, plus three 90-day signals to watch:

— Where the AWRP floor settles (and what that does to FRO)

— The Asian LNG margin compression window (JERA/KOGAS positioning)

— The DFC test event — and which direction it repriches the strait

For ZTrader.AI Research paying subscribers.

🔒 Subscribe to read →