The 10-Year Yield Myth: Is Bessent Forging the Narrative, or Playing the Prophet?

The war may explain the spike. It does not explain the floor.

Every Treasury selloff needs a story.

The fiscal bears call it a buyers’ strike. The administration calls it a temporary shock. Equity traders watch the 10-year yield cross another round number and treat it like the bond market has just issued a formal declaration of regime change.

Scott Bessent has chosen his story.

In May, with the 10-year Treasury yield near 4.67% and the 30-year near 5.18%, Bessent argued that elevated yields and the inflation pressure created by the energy shock were “transient.” His mechanism was straightforward: the Iran conflict would end, the Strait of Hormuz would reopen and energy prices would normalize.

He pointed to the oil curve as evidence. July Brent traded near $105, while December sat closer to $88. The market was pricing an acute near-term supply disruption, not permanently expensive oil. (Reuters)

It was a coherent argument.

It was also a remarkably convenient one for the man responsible for selling American debt.

Bessent is not forging the data.

He is forging the frame.

The question is not whether the geopolitical premium was real. It was.

The question is whether a real short-term shock is being used to explain away a much less comfortable long-term repricing.

That is where the myth begins.

One Yield, Several Markets

The bearish Treasury narrative often compresses several separate claims into one:

Higher oil means higher inflation.

Higher inflation means the Fed stays tighter.

Higher rates mean investors distrust the fiscal regime.

Higher yields therefore prove that Washington has lost control of the bond market.

Each step can be true.

The conclusion does not automatically follow from the catalyst.

The 10-year yield is not one price. It is a stack of prices.

At the simplest level:

10-year yield = expected short rates + term premium

Inside that term premium sit inflation uncertainty, real-rate risk, Treasury supply, liquidity, volatility and the compensation required to hold duration through a decade of political improvisation.

A higher 10-year yield can therefore mean several different things.

The market may expect the Fed to keep short rates higher.

It may demand more compensation for inflation risk.

It may demand a higher real return.

Or it may refuse to absorb long-duration supply at yesterday’s price.

These are different signals.

They are also different trades.

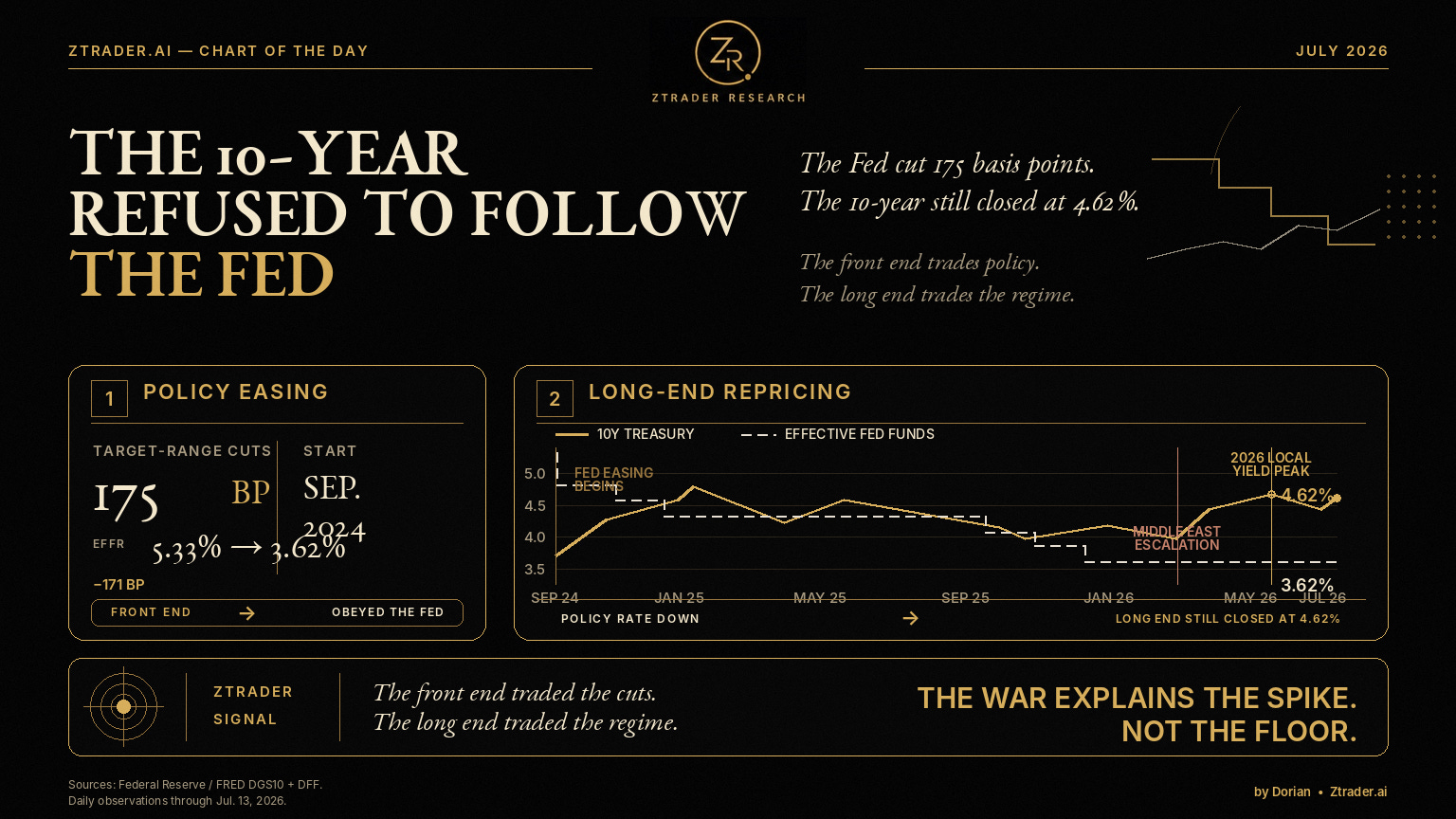

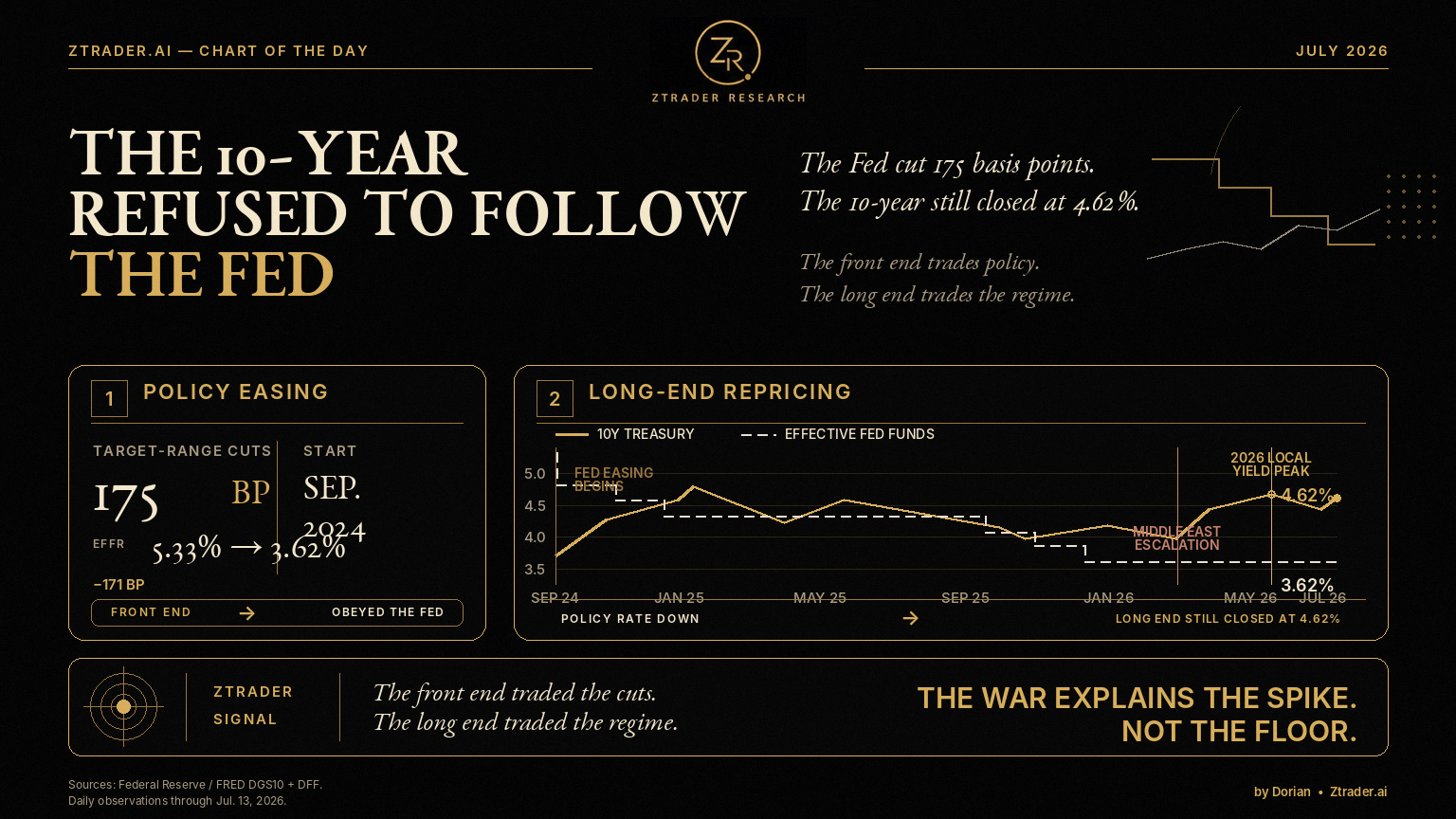

The Long End Stopped Obeying the Fed

The first myth is that the 10-year Treasury should mechanically follow the federal funds rate lower.

It did not.

The Fed cut its target rate by 175 basis points over roughly eighteen months, yet the 10-year yield continued to hover above 4%.

Federal Reserve researchers found that movements in far-forward rates help explain why the long end remained elevated despite policy easing.

This matters.

When the policy rate falls but the 10-year refuses to follow, the market is saying that easing the next few meetings does not eliminate the risks embedded in the next ten years.

The front end trades the Fed.

The long end trades the regime.

That regime includes fiscal supply, inflation volatility, real growth uncertainty and the price investors demand to warehouse duration.

Bessent can plausibly blame the conflict for accelerating the move.

He cannot plausibly blame the conflict for creating the entire yield floor.

CHART 01 — THE 10-YEAR REFUSED TO FOLLOW THE FED

Chart takeaway:

The Fed delivered 175 basis points of easing, but the 10-year remained above 4%. On July 13, the effective federal funds rate was 3.62%, while the constant-maturity 10-year yield was 4.62%. (FRED)

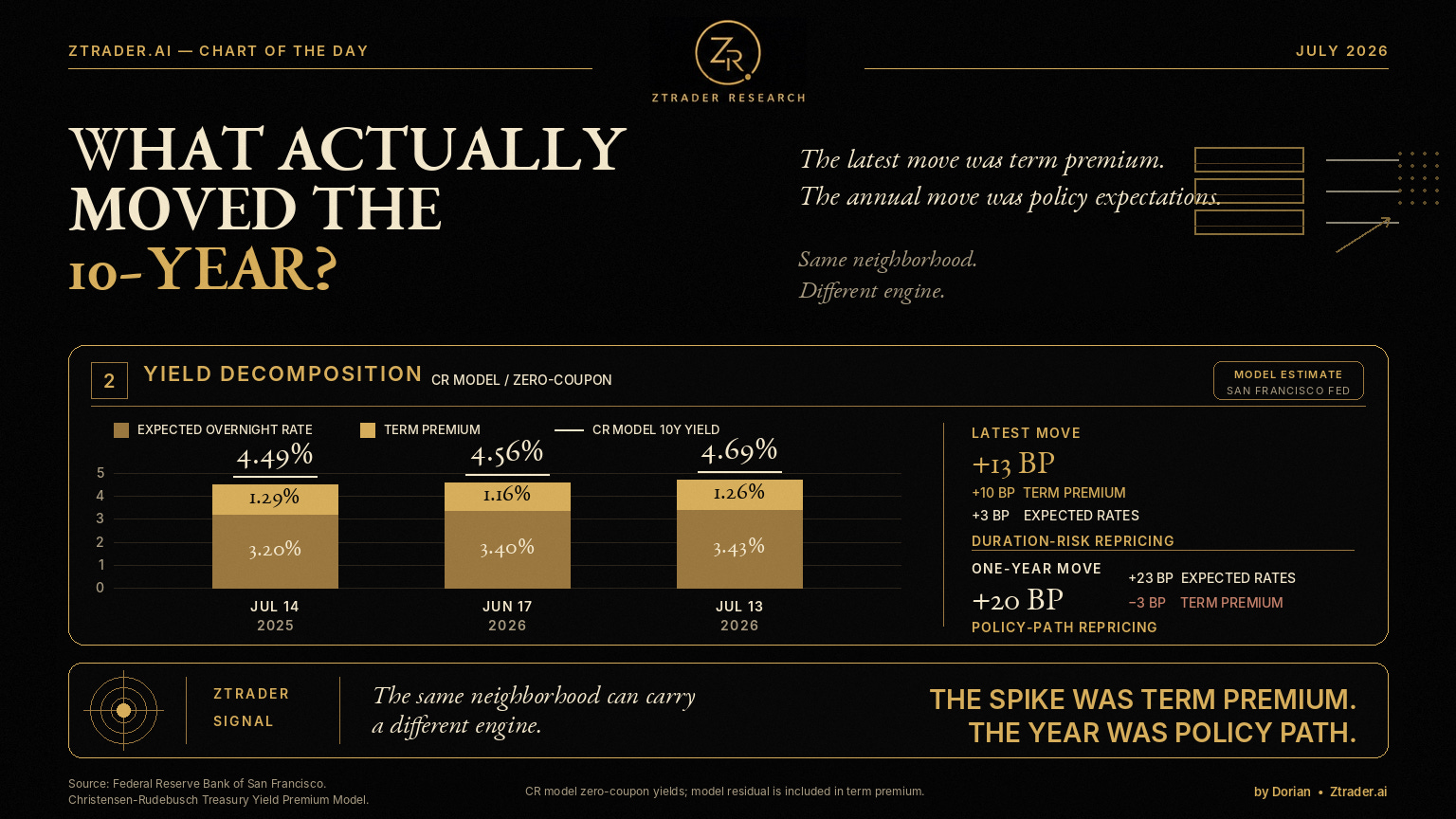

The Recent Spike Was Mostly Term Premium

The San Francisco Fed’s Christensen-Rudebusch model gives us a cleaner decomposition.

It divides the 10-year zero-coupon nominal Treasury yield into:

the average expected overnight rate over the next decade;

the 10-year term premium.

The model residual is included in the term-premium estimate so the components add up to the observed model yield. That means the decomposition is useful, but not divine revelation carved into a Bloomberg terminal. (Federal Reserve Bank of San Francisco)

On June 17, 2026:

CR model 10-year zero-coupon yield: 4.56%

Average expected overnight rate: 3.40%

Term premium: 1.16%

By July 13:

CR model 10-year zero-coupon yield: 4.69%

Average expected overnight rate: 3.43%

Term premium: 1.26%

The model yield rose 13 basis points.

Only 3 basis points came from a higher expected path for short-term rates.

Roughly 10 basis points came from a higher term premium.

Within the CR model, the latest selloff was therefore primarily a repricing of duration risk, not a major change in the expected overnight-rate path.

But widen the window.

On July 14, 2025:

CR model 10-year zero-coupon yield: 4.49%

Average expected overnight rate: 3.20%

Term premium: 1.29%

One year later, the model yield was 20 basis points higher, yet the term premium was 3 basis points lower.

Within the CR framework, the year-over-year rise was fully accounted for by a higher expected path for short-term rates, partly offset by a slightly lower term premium. (Federal Reserve Bank of San Francisco)

That gives us two valid conclusions.

The latest spike was mainly a term-premium event.

The broader one-year move does not support the simple claim that the entire rise was a term-premium-driven fiscal buyers’ strike.

Both can be true.

Markets retain this irritating ability to hold more than one idea at once.

CHART 02 — WHAT ACTUALLY MOVED THE 10-YEAR?

Chart takeaway:

The June-to-July increase came mostly from the estimated term premium. The year-over-year increase did not. (Federal Reserve Bank of San Francisco)

Inflation Is Not the Whole Story

Bessent’s best argument is not that inflation disappeared.

It clearly did not.

His better argument is that the market has not priced a permanent loss of inflation control.

The 10-year breakeven inflation rate stood at 2.25% on July 14. That is not especially low, but it is hardly evidence that long-run inflation expectations have broken loose. (FRED)

The June CPI report strengthened his case.

Headline CPI fell 0.4% month over month, the largest monthly decline since April 2020. Core CPI was unchanged.

Year-over-year headline inflation slowed from 4.2% to 3.5%, while core inflation fell from 2.9% to 2.6%.

The energy index declined 5.7% in June, also its largest monthly fall since April 2020, although energy prices remained 15.7% higher than a year earlier. (Bureau of Labor Statistics)

The energy shock was real.

The latest data did not show it spreading mechanically through the entire consumption basket.

The June FOMC minutes told a similar story.

The Fed noted that the nominal 10-year yield had risen around 50 basis points since the conflict began. Yet longer-term inflation expectations remained anchored, while the rise in nominal Treasury yields during the intermeeting period largely reflected higher real rates.

That distinction is the center of the trade.

The market is not necessarily saying:

The Fed has lost control of inflation.

It may instead be saying:

Keeping inflation under control will require higher real rates, more compensation for duration and a higher clearing price for fiscal supply.

The first message is a credibility crisis.

The second is a repricing of the cost of credibility.

CHART 03 — YIELD UP, BREAKEVENS CONTAINED

Chart takeaway:

Around the July 13–14 window, the nominal 10-year yield was roughly 4.62%, the real 10-year TIPS yield was 2.36%, and the 10-year breakeven rate was about 2.25%. The pressure was concentrated in real yields rather than an unanchoring of long-term inflation compensation. (FRED)

The Spike Can Fade Without Solving the Floor

This is where Bessent’s argument becomes credible and misleading at the same time.

He may be right about the spike.

Oil can fall.

Near-term inflation compensation can decline.

The Fed can regain room to ease.

The term premium can retrace as volatility falls and investors rebuild duration exposure.

If that happens, the 10-year could fall materially from its recent highs. Bessent would appear prophetic.

But a tactical duration rally would not prove that the structural problem had disappeared.

It would prove only that the market removed the geopolitical surcharge.

The deeper issue sits in far-forward real risk.

Federal Reserve research finds that the rise in far-forward Treasury rates over recent years was not driven by higher long-run inflation expectations or inflation risk.

Instead, the increase was concentrated in the far-forward real risk premium.

The Fed estimates that the total far-forward risk premium now sits near its 85th percentile since 1971. It has risen by roughly 200 basis points over the past several years, with the increase attributed entirely to the real component.

The paper identifies renewed adverse-supply-shock risk and concern over future federal deficits as plausible drivers.

That is not a temporary oil trade.

It is the market demanding compensation for a world in which future capital may be scarcer, fiscal flexibility weaker and government-debt supply larger.

Bessent explains the spike because the spike is reversible.

He avoids explaining the floor because the floor belongs to the fiscal regime.

The Fiscal Arithmetic Is Not a Myth

The United States is not facing an imminent Treasury funding crisis.

That does not mean investors must lend to it cheaply.

The Congressional Budget Office projects a federal deficit of $1.9 trillion in fiscal 2026, equal to 5.8% of GDP. By 2036, the deficit is projected to reach $3.1 trillion, or 6.7% of GDP.

Debt held by the public is projected to rise from 101% of GDP in 2026 to 120% by 2036. Rising net interest costs drive much of the deterioration.

This matters through supply.

Treasury does not need to lose access to capital for yields to rise.

It only needs to issue more duration than investors are willing to absorb at the previous clearing price.

The dramatic version of the fiscal crisis imagines an empty auction room.

The more realistic mechanism is less cinematic:

Buyers still arrive.

They simply demand a higher yield.

May’s Data Showed No Foreign Buyers’ Strike

The latest available TIC data, covering May, showed no broad foreign retreat from Treasury notes and bonds.

Foreign private investors purchased a net $53.6 billion during the month. Foreign official institutions added another $3.0 billion, bringing total net foreign purchases to $56.6 billion.

Over the twelve months through May, private foreign investors purchased a net $324.4 billion, while official institutions sold a net $34.0 billion. Combined net foreign purchases were therefore approximately $290.4 billion.

Foreign residents also purchased a net $262.8 billion of long-term U.S. securities across Treasuries, agency debt, corporate bonds and equities during May. (U.S. Department of the Treasury)

As of May, this was not a foreign buyers’ strike.

But it was not evidence of infinitely price-insensitive demand either.

The Fed noted that Treasury ownership has shifted somewhat from relatively price-insensitive official-sector holders toward more price-sensitive private investors, a change that may affect the term premium.

A foreign central bank accumulating reserves may buy Treasuries because it has a policy reason to do so.

A hedge fund, insurer, bank or asset manager buys because the expected return compensates for duration, volatility, funding and balance-sheet use.

Demand has not disappeared.

Its reservation price has changed.

The TIC data also require caution. Treasury notes that the figures are largely based on custodial records and cannot always identify the true beneficial owner of a security. They are useful evidence, not omniscient surveillance of every foreign bond portfolio. (U.S. Department of the Treasury)

The Real Myth

The real myth is not Bessent’s claim that the war premium can reverse.

Of course he can.

The myth is that reversing the war premium returns the Treasury market to its old equilibrium.

It does not.

The old equilibrium depended on several favorable conditions:

Low and stable inflation.

Low Treasury supply relative to structural demand.

Heavy official-sector reserve accumulation.

A compressed or negative term premium.

An investor base willing to treat long-duration Treasuries as automatic protection against every risk-asset drawdown.

Those conditions have weakened.

The market can believe the Fed will ultimately contain inflation while demanding a higher real return for financing the government.

There is no contradiction.

Fed credibility can survive.

Cheap duration can still die.

The Trade Map

The correct position is not built around whether Bessent is honest.

It is built around which component of the yield moves next.

Scenario 1 — Bessent the Prophet

Oil falls.

Breakeven inflation remains contained.

The term premium retraces.

The 10-year breaks below 4.50%.

This is a tactical duration rally driven by the removal of the geopolitical premium.

Trade expression: Long duration / bull-flattening bias.

Invalidation: Oil stabilizes lower, but real yields and the term premium continue rising.

Scenario 2 — The Structural Floor Holds

Oil and headline CPI fall, but the 10-year remains trapped around 4.50% to 4.75%.

That would confirm that the conflict was a catalyst, not the regime.

Fiscal supply and far-forward real risk would remain embedded in the curve.

Trade expression: Fade aggressive duration rallies / retain a conditional steepening bias.

Invalidation: The term premium compresses decisively while auction demand strengthens across several cycles.

Scenario 3 — Inflation Repricing Returns

The 2-year yield, 10-year breakeven and nominal 10-year yield rise together.

That would signal something more dangerous than a pure duration-risk shock.

The market would be repricing the Fed path, inflation persistence and real rates at the same time.

Trade expression: Avoid premature duration longs / favor front-end rate volatility.

Invalidation: Breakevens reverse while nominal yields remain high, shifting the move back toward real yield.

Scenario 4 — The Actual Vigilante Signal

Oil falls.

Long-term inflation expectations stay anchored.

Yet the 10-year pushes toward 5%.

Treasury auctions tail repeatedly.

Dealer absorption rises.

Foreign and domestic real-money demand weakens.

That would be the genuine warning.

Not that nobody wants Treasuries.

That buyers now require a structurally higher clearing yield.

Final Judgment

Bessent is neither a pure mythmaker nor a clean prophet.

He is managing attribution.

He takes a visible, reversible shock and places it at the center of the yield story. That protects Treasury-market credibility and discourages a cyclical selloff from becoming a fiscal referendum.

The evidence partly supports him.

The oil curve priced normalization.

Long-term inflation compensation remained contained.

Core CPI did not accelerate in June.

Foreign demand for Treasury notes and bonds had not disappeared as of May.

But the structural message remains.

The United States has not lost access to capital.

It has lost access to cheap duration.

The war may explain the spike.

It does not explain the floor.