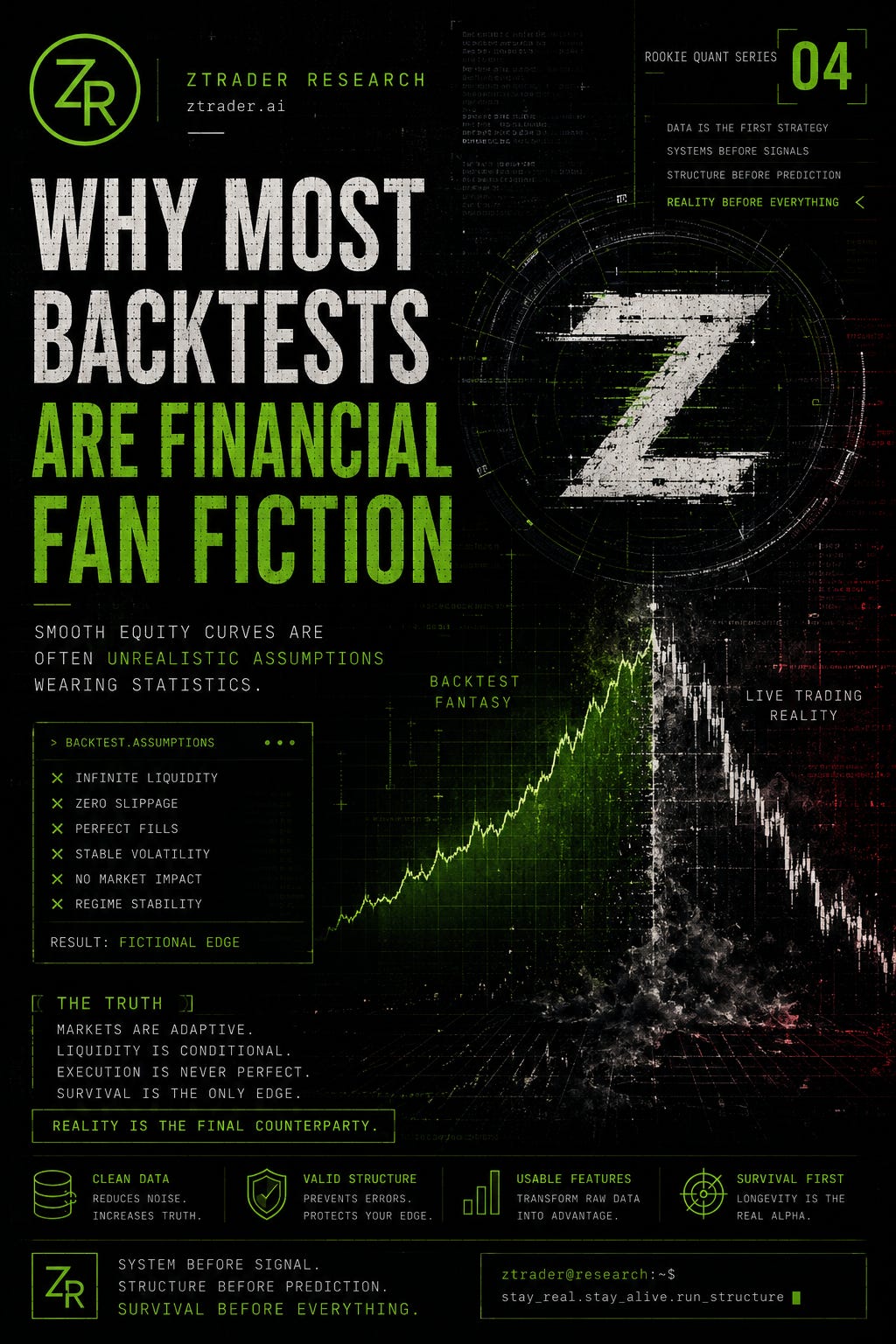

Rookie Quant Series 04: Why Most Backtests Are Financial Fan Fiction

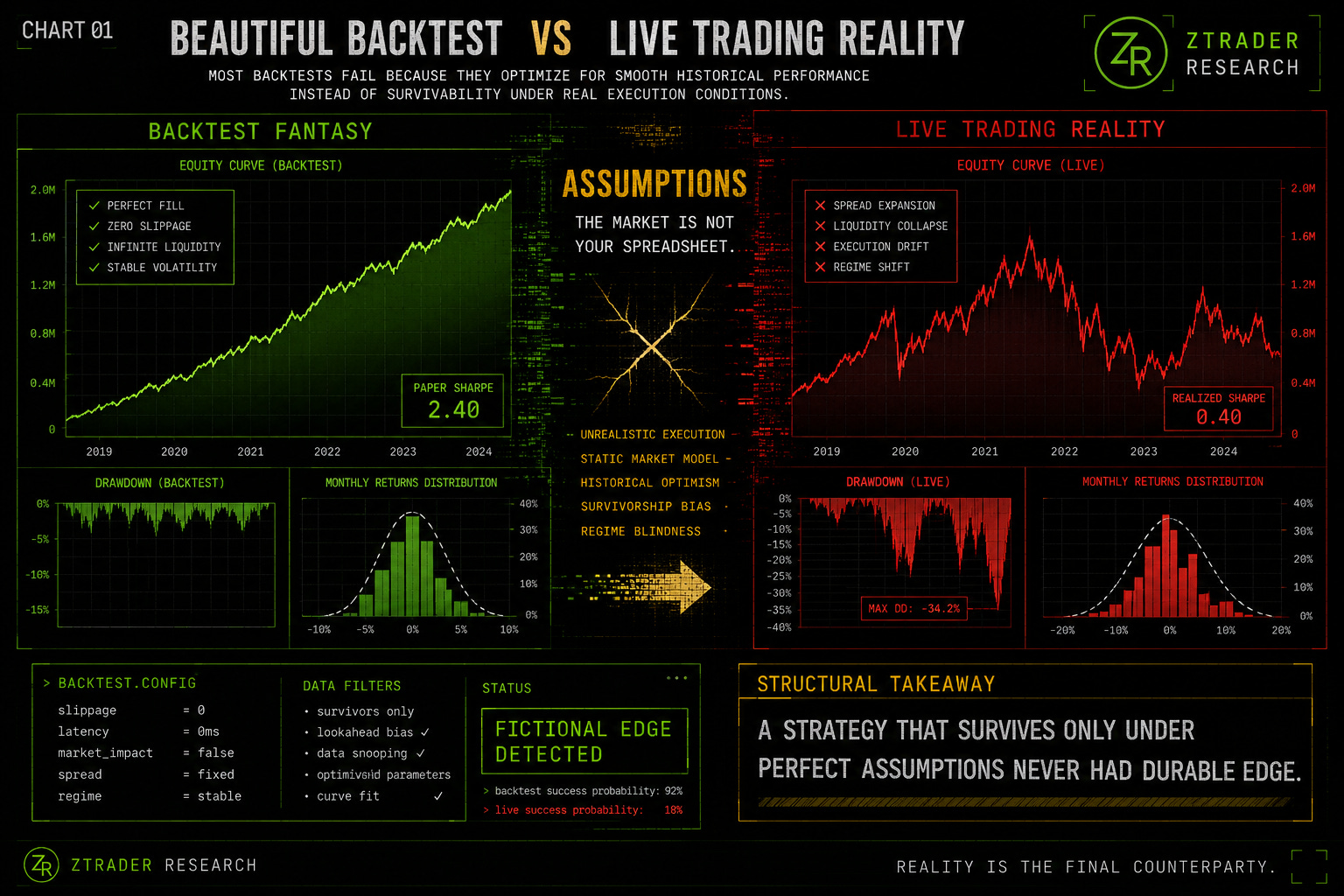

Smooth equity curves are among the most dangerous visual objects in finance.

Because smooth backtests often hide fragile assumptions.

Most beginner traders do not fall in love with the strategy itself.

They fall in love with the curve.

The equity line rises steadily. Drawdowns remain shallow. The Sharpe ratio looks elegant. The returns appear stable and intelligent.

For a brief moment, it feels like discovering hidden truth inside the market.

Then live trading begins.

And reality arrives like a lawsuit from physics.

The Core Problem

Most people think a backtest tests reality.

It does not.

A backtest tests assumptions about reality.

Every backtest silently assumes things like:

liquidity exists

spreads remain stable

fills are achievable

volatility behaves normally

execution happens instantly

market structure stays compatible

The problem is that markets are adaptive systems.

Reality does not care about your spreadsheet.

This is why many retail strategies perform beautifully historically and collapse immediately once deployed live.

The strategy was never detecting durable market structure.

It was detecting a fragile set of assumptions.

The Seduction of Smooth Curves

Humans are biologically vulnerable to smooth upward lines.

Smoothness creates emotional trust.

The cleaner the equity curve appears, the more believable the system feels.

This creates one of the largest psychological traps in modern quant culture:

visual stability gets mistaken for structural robustness.

But many smooth backtests are simply the result of unrealistic assumptions:

perfect fills

frictionless execution

infinite liquidity

stable volatility

no market impact

no regime instability

The more unrealistic the assumptions become, the more beautiful the backtest often looks.

Civilization itself is basically a multi-thousand-year attempt to emotionally stabilize around charts.

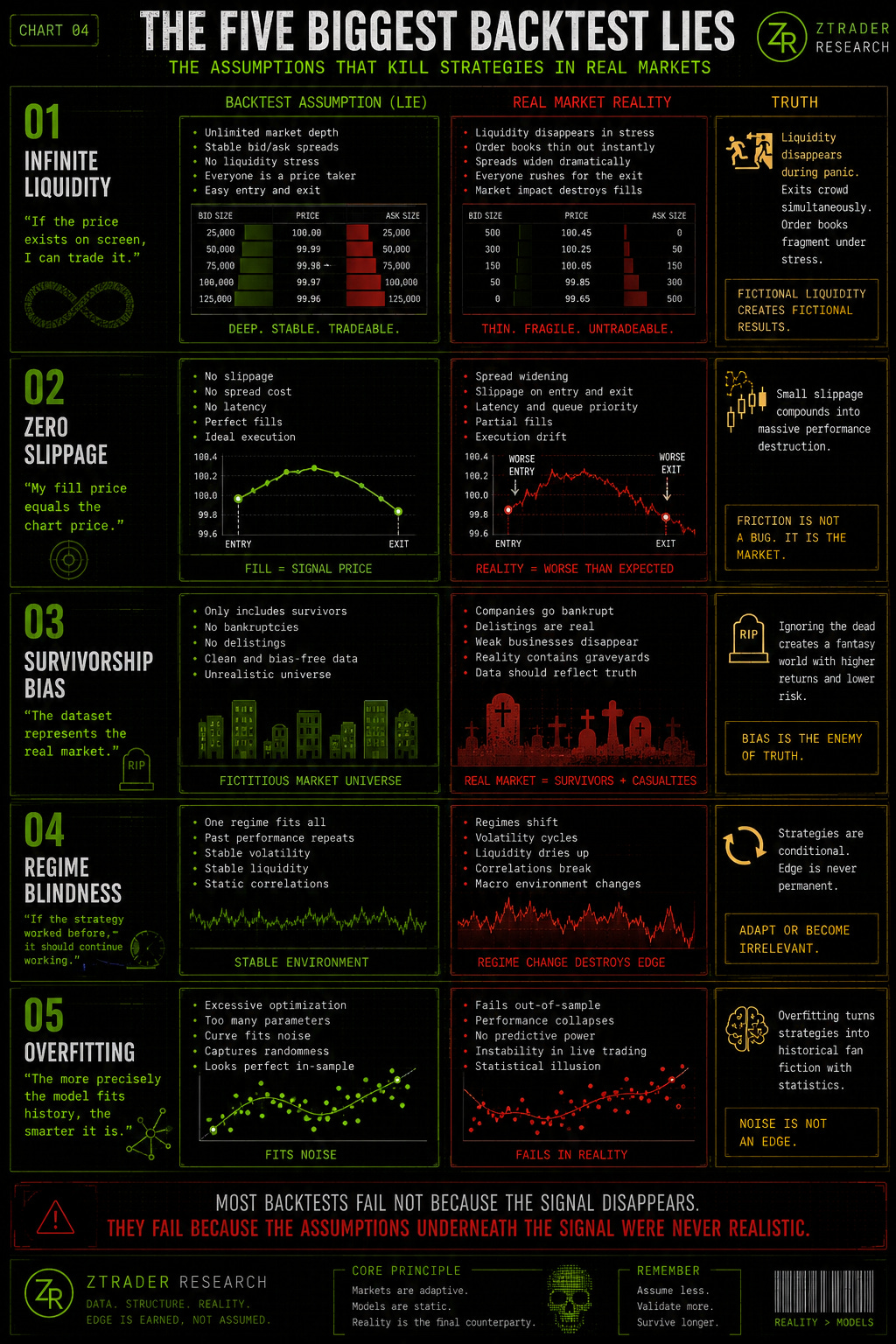

The Five Biggest Backtest Lies

01. Infinite Liquidity

Most retail backtests assume you can always enter and exit positions at displayed prices.

Real markets disagree.

Liquidity is conditional.

Liquidity is emotional.

It disappears precisely when:

fear rises

volatility expands

exits become crowded

leverage unwinds

positioning becomes one-sided

A strategy requiring stable liquidity during unstable conditions is not robust.

It is conditional fantasy.

02. Zero Slippage

Most beginner systems treat execution friction as negligible.

Professional desks treat execution friction as survival-critical.

During fast markets:

spreads widen

fills deteriorate

latency matters

order books thin out

volatility distorts price discovery

Tiny slippage assumptions can destroy entire strategies.

Especially in:

options

crypto

small-cap equities

overnight sessions

earnings events

macro releases

A strategy that only survives under ideal execution conditions never had durable edge in the first place.

03. Survivorship Bias

Many datasets quietly remove dead companies.

This creates a fictional universe where weak businesses never existed.

Reality contains bankruptcy.

Reality contains collapse.

Reality contains graveyards.

Your dataset should too.

Otherwise the system is not studying markets.

It is studying historical winners selected by hindsight.

04. Regime Blindness

A strategy that worked during:

QE

low volatility

passive inflow expansion

strong liquidity

…may completely fail during:

tightening cycles

inflation shocks

volatility expansion

liquidity stress

macro uncertainty

Retail behavior tends to assume strategy permanence.

Market structure does not.

Every edge is conditional.

05. Overfitting

Overfitting is what happens when intelligence loses contact with reality.

The system stops identifying repeatable behavior.

Instead, it memorizes historical accidents.

At that point, the strategy is no longer a model.

It becomes:

historical cosplay with statistics.

The backtest looks intelligent because the system has already seen the answers.

Reality does not provide answer keys in advance.

The Retail Quant Illusion

Retail quant culture often optimizes for elegance instead of survivability.

Beginners obsess over:

indicators

entries

parameter optimization

AI buzzwords

model complexity

Professionals obsess over:

execution

exposure

liquidity

volatility

drawdown

stress behavior

regime dependency

Because professional trading is not primarily about prediction.

It is about surviving uncertainty.

A mediocre strategy with realistic assumptions often outperforms a mathematically beautiful strategy built on fantasy conditions.

This is why institutional systems frequently look:

slower

uglier

less profitable

more conservative

…and significantly more durable.

Professional research is not designed to create emotional excitement.

It is designed to survive contact with reality.

Why AI Makes This Worse

AI has dramatically lowered the barrier to strategy generation.

Now almost anyone can generate:

indicators

trading systems

optimization scripts

backtests

ML pipelines

This creates a dangerous illusion of sophistication.

Because generating signals is no longer difficult.

Structural honesty is difficult.

Many AI-generated systems quietly ignore:

execution degradation

liquidity instability

volatility clustering

regime shifts

market impact

position crowding

This creates entire ecosystems of synthetic intelligence.

Systems that appear intelligent until they encounter actual markets.

And actual markets are extremely hostile environments.

The Market Is Not Your Spreadsheet

Markets are not static equations.

They are adaptive systems driven by:

fear

leverage

positioning

liquidity stress

reflexivity

forced behavior

The moment enough participants discover the same edge, the environment changes.

This is why:

edges decay

strategies crowd

execution deteriorates

volatility regimes shift

Reality continuously updates itself.

Your system must survive those updates.

In the premium section we go deeper into:

how slippage silently destroys Sharpe ratios

why volatility regimes invalidate historical edge

the hidden mathematics of drawdown fragility

how professional desks stress-test systems

why execution quality matters more than most signals

how fake alpha is accidentally manufactured

what realistic institutional backtesting actually looks like

The difference between retail backtests and professional research is rarely mathematics.

It is usually contact with reality.