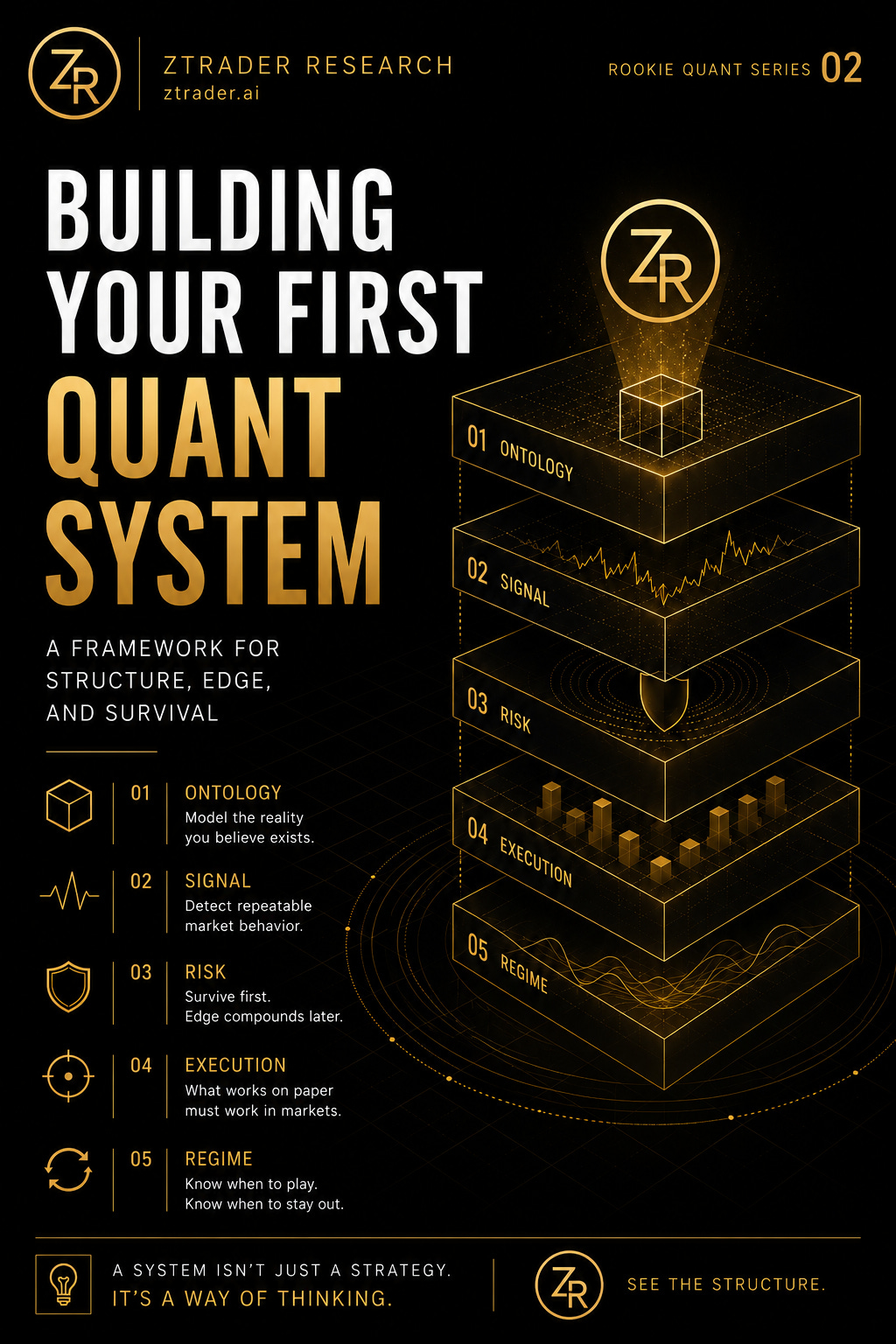

Rookie Quant Series 02: Building Your First Quant System (Without Lying to Yourself)

Most people think building a quant system means writing indicators and backtesting charts.

It doesn’t.

Most beginner quant systems are simply:

historical fan fiction with Python syntax.

Because hindsight is addictive.

Once humans see what already happened, the brain immediately starts constructing explanations that feel intelligent:

“This setup was obvious.”

“…