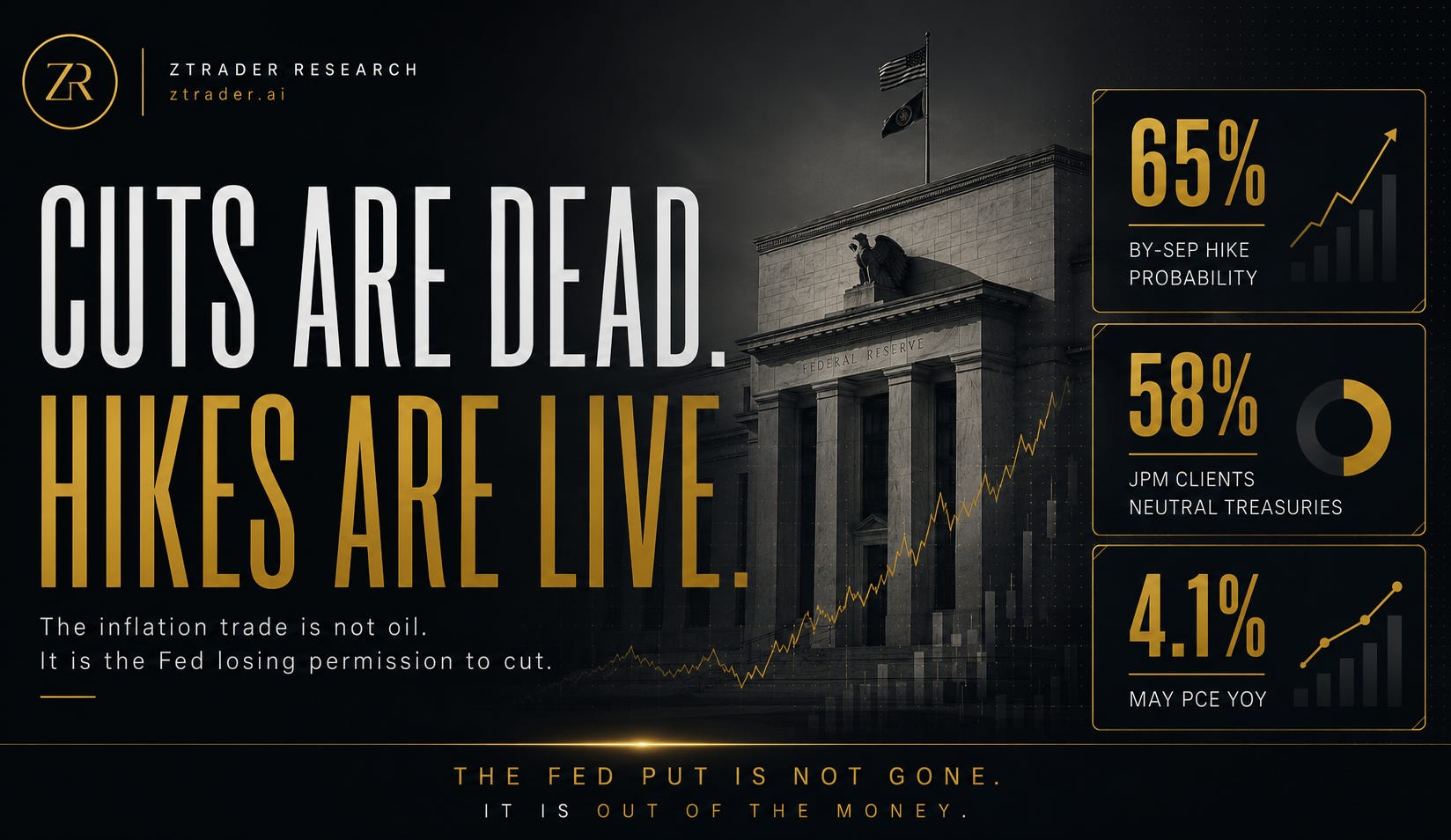

FED Cuts Are Dead. Hikes Are On Its Way

The inflation trade is not oil. It is the Fed losing permission to cut.

The question is not whether the Fed will launch a full hiking cycle.

That is the wrong frame.

The better question is simpler:

What if the Fed does not need to hike much for the market to suffer? What if it only needs to be unable to cut?

That is the regime shift.

For most of the year, the market’s hidden operating system was built around one assumption:

inflation fades / growth cools / Fed cuts / duration works / risk survives.

That system is now corrupted.

Not destroyed.

Corrupted.

The market has not priced a clean hiking cycle. It has priced the death of the old easing path. Hikes moved from tail risk into live risk. Cuts moved from base case into wishful thinking. Duration went from consensus comfort trade into something managers now hold with gloves on.

The Fed did not need to scream.

It only needed to stop comforting the market.

The June FOMC statement held the target range at 3.50%–3.75%, but it also said inflation remained elevated relative to the Committee’s 2% goal and that the Committee would deliver price stability. That is not a cutting setup. That is a central bank refusing to give the market a pillow.

The old question was:

When will the Fed cut?

The new question is:

What if the Fed cannot?

That is where the trade begins.

What the market believed

The market believed the inflation scare was temporary.

Not irrationally.

Oil spiked.

Middle East risk widened.

Energy passed through headline inflation.

Then oil began to cool.

So the clean consensus became: headline inflation will fade, the Fed will look through the shock, and cuts can come back into the conversation.

That view is not wrong,

It’s incomplete.

Because the Fed does not set policy only on headline oil math. It sets policy inside a credibility problem.

If headline falls but core stays sticky, the Fed does not get a clean cutting signal.

If services inflation refuses to break, the Fed does not get permission to rescue duration. If inflation stays visibly above target, the Fed cannot safely behave like an equity-volatility suppression machine, which is tragic news for a market addicted to adult supervision.

This is the missing layer:

The inflation trade is no longer just energy. This is the policy constraint trade.

What changed

The repricing started in the front end.

Reuters reported on June 16 that U.S. rate futures priced a 64% chance of a Fed hike by the December meeting, up from 24% one month earlier. That is not a minor forecast adjustment. That is the market deleting the “cuts are coming” template and replacing it with something uglier. (Reuters)

Then the May PCE report hit.

July was still not the clean meeting. Reuters reported that markets priced only about a 30% probability of a July hike. But September became live, with markets pricing about an 80% probability of a hike at the September meeting.

That distinction matters.

July low / September live.

No panic / but no easing path.

No full hiking cycle / but no free duration rescue.

That is the first chart.

CHART 01

The real move is not probability. It is permission.

People obsess over the exact hike probability.

65%.

80%.

62%.

Whatever the latest article-time snapshot says.

That is useful, but it is not the deepest signal.

Fed funds probabilities move intraday. They jump around with oil, PCE, payrolls, headlines, and whatever new delusion the market downloads before lunch.

The regime signal is not the exact number.

The regime signal is this:

The market now has to price a Fed that may not have permission to cut.

That breaks the old chain.

Cuts removed means duration loses its automatic bid.

Duration losing its automatic bid means long-duration equities lose part of their valuation oxygen.

Higher front-end uncertainty means curve trades become more unstable.

More policy uncertainty means term premium becomes harder to suppress.

And every crowded trade built on lower discount rates has to ask whether the floor is still there.

The Fed may hike.

But the larger trade is that the Fed may not be able to ease.

That is enough.

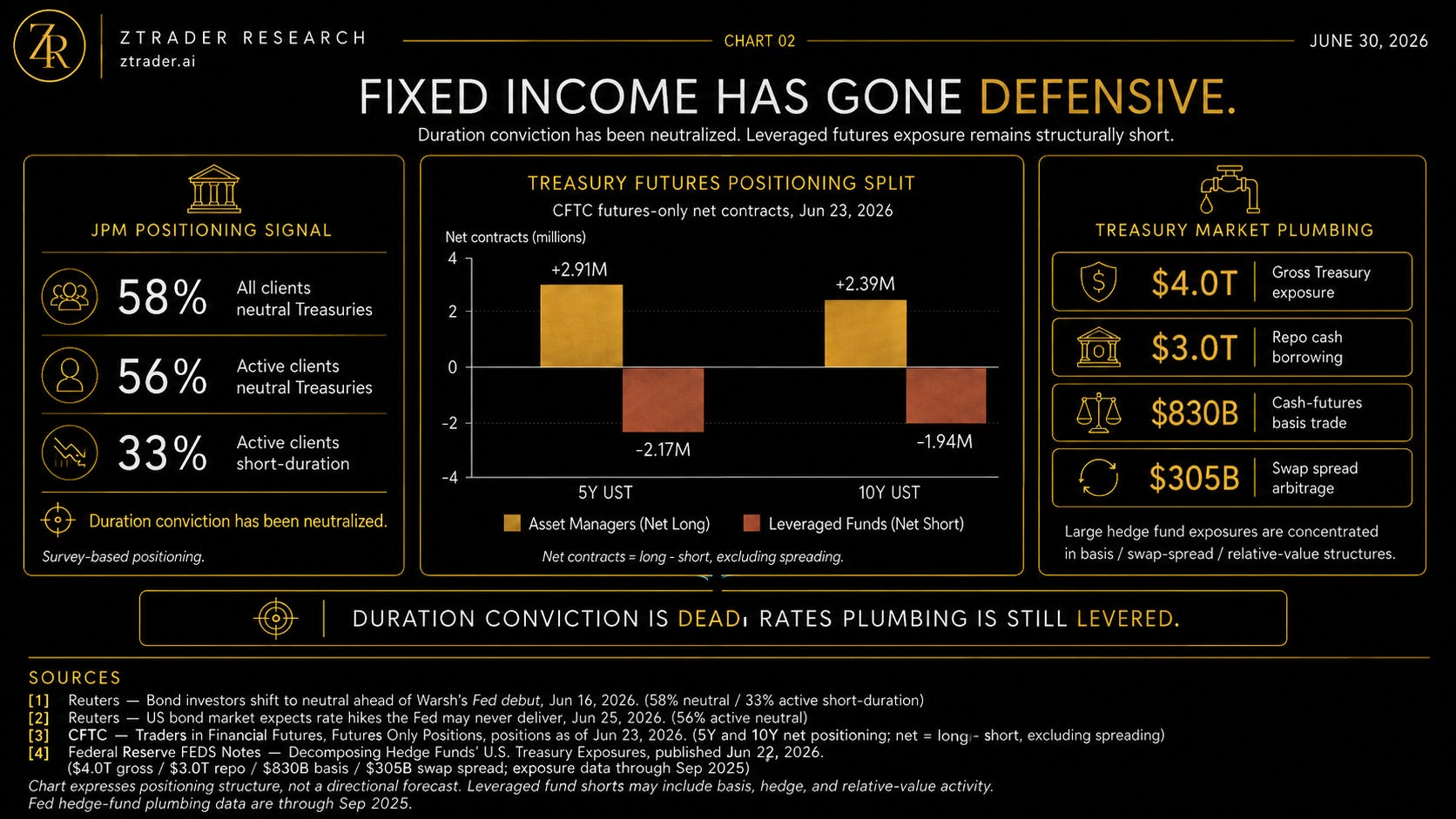

Fixed income already got the message

The bond market did not respond by screaming “short everything.”

That would be too easy. And rates are never easy, because apparently finance needed one asset class where even being right directionally can still bankrupt you.

The signal is cleaner:

Duration conviction has been neutralized.

Reuters reported that J.P. Morgan’s Treasury Client Survey showed neutral Treasury positioning rising to 58% among all clients, while short-duration positioning among active clients rose to 33%. (Reuters)

That is not euphoric long-duration behavior.

That is defense.

Real money may still own duration. Asset managers may still be structurally long Treasuries. But the psychological position has changed.

The old trade was:

buy duration before cuts.

The new trade is:

do not get caught concentrated in duration if the Fed cannot cut.

That is the second chart.

CHART 02

The plumbing matters more than the headline

Rates positioning is not just a macro opinion.

It is plumbing.

Treasuries are collateral.

Treasury futures are hedge instruments.

Repo is balance sheet.

Basis is leverage.

Swap spreads are shadow duration.

And hedge funds sit inside the machinery, not outside it.

CFTC futures-only data as of June 23 showed asset managers net long roughly +2.91 million 5-year Treasury futures contracts and +2.39 million 10-year contracts. Leveraged funds were net short roughly -2.17 million 5-year contracts and -1.94 million 10-year contracts, calculated as long minus short, excluding spreading.

Do not misread this.

Leveraged fund shorts are not automatically a pure directional “bonds go down” bet.

Some of it is basis.

Part of it is hedge.

Part of it is relative value.

Some of it is funding structure wearing a macro costume.

That is exactly why it matters.

When Fed risk changes, it does not just move a yield chart. It moves the machine:

front-end pricing / Treasury futures / repo / basis economics / swap spreads / balance-sheet appetite / real-money duration tolerance.

The Fed’s own work shows how large this machine has become. A June 2026 FEDS Note found large hedge funds’ gross Treasury exposures had doubled to $4.0 trillion by September 2025, including $2.4 trillion long and $1.6 trillion short exposure.

Repo cash borrowing reached $3.0 trillion, while the Treasury cash-futures basis trade reached about $830 billion and swap-spread arbitrage about $305 billion.

That data is through September 2025, not a June 2026 live position.

But it tells you what kind of market this is.

Not a clean bond market.

A levered rates system.

So when inflation becomes live again, the stress does not travel politely.

It travels through plumbing.

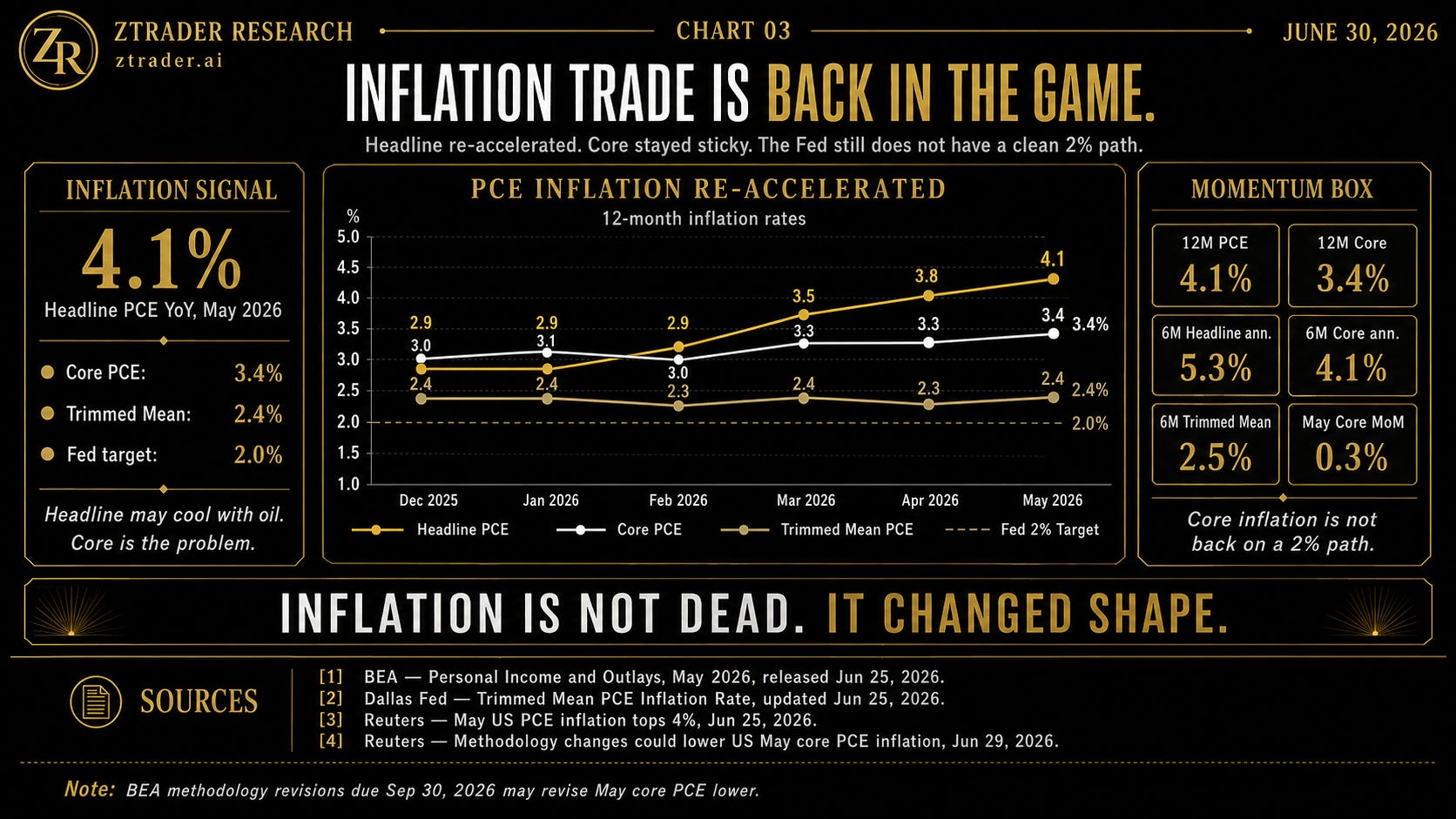

Inflation is not dead. It changed shape.

The market wants inflation to be one variable.

Oil up: inflation.

Oil down: no inflation.

Cute. Wrong enough to be expensive.

May PCE gave the market a more annoying message. BEA reported that the PCE price index rose 0.4% month-over-month and 4.1% year-over-year in May. Core PCE rose 0.3% month-over-month and 3.4% year-over-year.

Dallas Fed’s trimmed mean PCE table showed the same headline/core problem from another angle: May 12-month headline PCE at 4.1%, core PCE at 3.4%, and trimmed mean at 2.4%. The trimmed mean is calmer, but calmer is not the same as back to 2%. (dallasfed.org)

This is the third chart.

The inflation trade is not oil

Oil matters.

But oil is not the whole trade.

The better framework:

Headline inflation is the trigger. Core persistence is the trap.

If oil cools, headline may fall.

That helps the no-hike camp.

It reduces immediate pressure.

It lets economists argue the shock is temporary.

It gives the Fed an excuse to wait.

But it does not automatically restore cuts.

Because cuts require more than lower oil. Cuts require confidence that inflation is moving back toward target.

That is where core matters.

Reuters reported that May PCE inflation broke above 4%, leaving a Fed hike on the table, while also noting that falling fuel prices could bring relief. That is the entire contradiction in one sentence: oil may cool the headline, but the Fed still has to explain why it would cut with core inflation at 3.4%. (Reuters)

The market is treating oil as the headline shock.

The Fed has to treat core as the credibility problem.

That gap is the trade.

The revision caveat

There is one real caveat.

BEA methodology updates scheduled for September 30, 2026 may revise May core PCE lower. Reuters reported Goldman economists estimated May core PCE year-over-year could be revised from 3.4% to 3.2%, while JPMorgan expected a smaller revision to 3.3% after rounding. (Reuters)

That matters.

But it does not kill the setup.

3.2% core PCE is not 2%.

3.3% core PCE is not 2%.

A lower revision can reduce hike urgency.

It does not restore a clean cutting regime.

That is the whole point.

The market does not need inflation to explode for duration to struggle.

Inflation only has to remain sticky enough to deny the Fed permission to ease.

The mechanism

Here is the full mechanism in one chain:

inflation persistence

/ Fed cannot validate cuts

/ front-end stays unstable

/ duration conviction weakens

/ leveraged rates plumbing absorbs volatility

/ term premium becomes harder to suppress

/ long-duration equity multiples lose oxygen

/ inflation-linked trades become investable again

This is not a 1970s rerun.

It is not “buy every commodity.”

It is not “short all bonds.”

That is the kindergarten version.

The real version:

The market is repricing the option value of Fed relief.

That option used to be valuable.

If growth slowed, the Fed could cut.

If equities cracked, the Fed could soften.

If duration puked, the Fed could guide.

If volatility rose, the Fed could talk the market down.

Now inflation blocks that function.

The Fed put is not gone.

It is out of the money.

The Decision layer

What would make me more bullish on the inflation trade?

Core PCE holding above 3%.

Services inflation refusing to soften.

Wage growth staying firm.

Energy cooling without core cooling.

Fed officials keeping price stability language hard.

Front-end hike probability staying live even after oil relief.

Treasury clients remaining neutral / short-duration instead of rebuilding duration conviction.

What would weaken the thesis?

Core PCE revising sharply lower.

Trimmed mean moving decisively toward 2%.

Services inflation breaking.

Oil relief transmitting into inflation expectations.

Fed officials rebuilding a cutting bias.

Real money adding duration aggressively.

Front-end hike pricing collapsing without a growth scare.

This is the trade filter.

Not vibes.

Not “macro feels hot.”

Not some heroic inflation call written by a guy who just discovered breakevens.

A regime has to keep proving itself.

Market expression

The cleanest expression is not one trade.

It is a map.

Rates:

front-end repricing / curve flattening during hawkish windows / less confidence in long-duration rallies.

Bonds:

avoid lazy long-duration conviction unless core inflation actually breaks.

Equities:

watch high-multiple duration. AI can remain structurally right and still get valuation pressure from rates. Good story / worse discount rate / messy price.

Commodities:

do not confuse oil shock with inflation regime. Energy can cool while core keeps the Fed trapped.

Breakevens / real assets:

the trade is resilience, not panic. Inflation protection matters most when the Fed cannot credibly declare victory.

Dollar:

rate differentials matter again if Fed hike risk stays live while other central banks debate relief.

The market is not asking whether inflation is scary enough for panic.

It is asking whether inflation is sticky enough to block rescue.

That is a much lower threshold.

And a much better trade.

Final thesis

The market has quietly completed the first repricing.

Cuts are no longer the base case.

Hikes are live.

Fixed income has gone defensive.

Rates plumbing is still levered.

Inflation is back as an investable regime.

But the trade is not “Fed hiking cycle.”

That is too blunt.

The trade is:

policy constraint.

The Fed may not need to hike aggressively for the market to suffer.

It only needs to be unable to cut.

That is why the second half matters.

The old market asked:

When will the Fed cut?

The new market asks:

What if the Fed cannot?