Book Of BlackSwan 01: There Is No Ordinary Event

Why Black Swans Are Usually Visible Before They Become Obvious

Ztrader Research · Black Swan Market Intelligence Series

Article 01

Most traders use the phrase “black swan” badly.

They use it to describe an event nobody could predict.

A pandemic/war.

A bank failure or flash crash.

Or Even a sovereign bond panic.

That definition is comforting because it makes failure look innocent.

Nobody could see it coming.

Nobody could prepare.

Nobody is responsible.

Markets love that story because it protects the ego of the crowd.

But in financial markets, the event is rarely the real black swan.

The event is only the match.

The real black swan is the structure that allows one match to burn down the whole building.

A virus does not automatically break the Treasury market.

A fiscal announcement does not automatically break pension funds.

A bank deposit outflow does not automatically become a systemic panic.

A war headline does not automatically become an oil shock, inflation shock, and volatility shock.

The damage happens when a visible risk enters a system full of hidden leverage, forced sellers, fragile funding, bad liquidity assumptions, crowded positioning, and policy delay.

That is the core thesis of this series:

A black swan is not simply an unknowable event. It is a mispriced fragility.

The trigger may be surprising.

The structure usually is not.

The Market Does Not Break From The Headline

The popular definition of a black swan focuses on surprise.

That is useful for philosophy.

It is less useful for trading.

Markets do not pay you for saying “nobody knew.”

Markets pay you for understanding where the system is fragile before the crowd is forced to care.

The better question is not:

What will the next black swan be?

The better question is:

Where can a normal shock create abnormal liquidation?

That is the difference between headline thinking and market structure thinking.

Headline thinking asks:

What happened?

Structure thinking asks:

Who is forced to trade because of what happened?

That second question is where the edge begins.

When a market breaks, price is not only expressing new information.

It is expressing balance sheet pressure/ collateral stress.

It is expressing dealer hedging/ redemption pressure.

It is expressing the distance between theoretical liquidity and real exit capacity.

This is why the same headline can produce radically different outcomes across regimes.

A war headline in a liquid, under-positioned, policy-flexible market may create a short shock and then fade.

The same headline in a crowded, leveraged, inflation-constrained market can trigger a multi-asset repricing.

The event is visible.

The fragility is the edge.

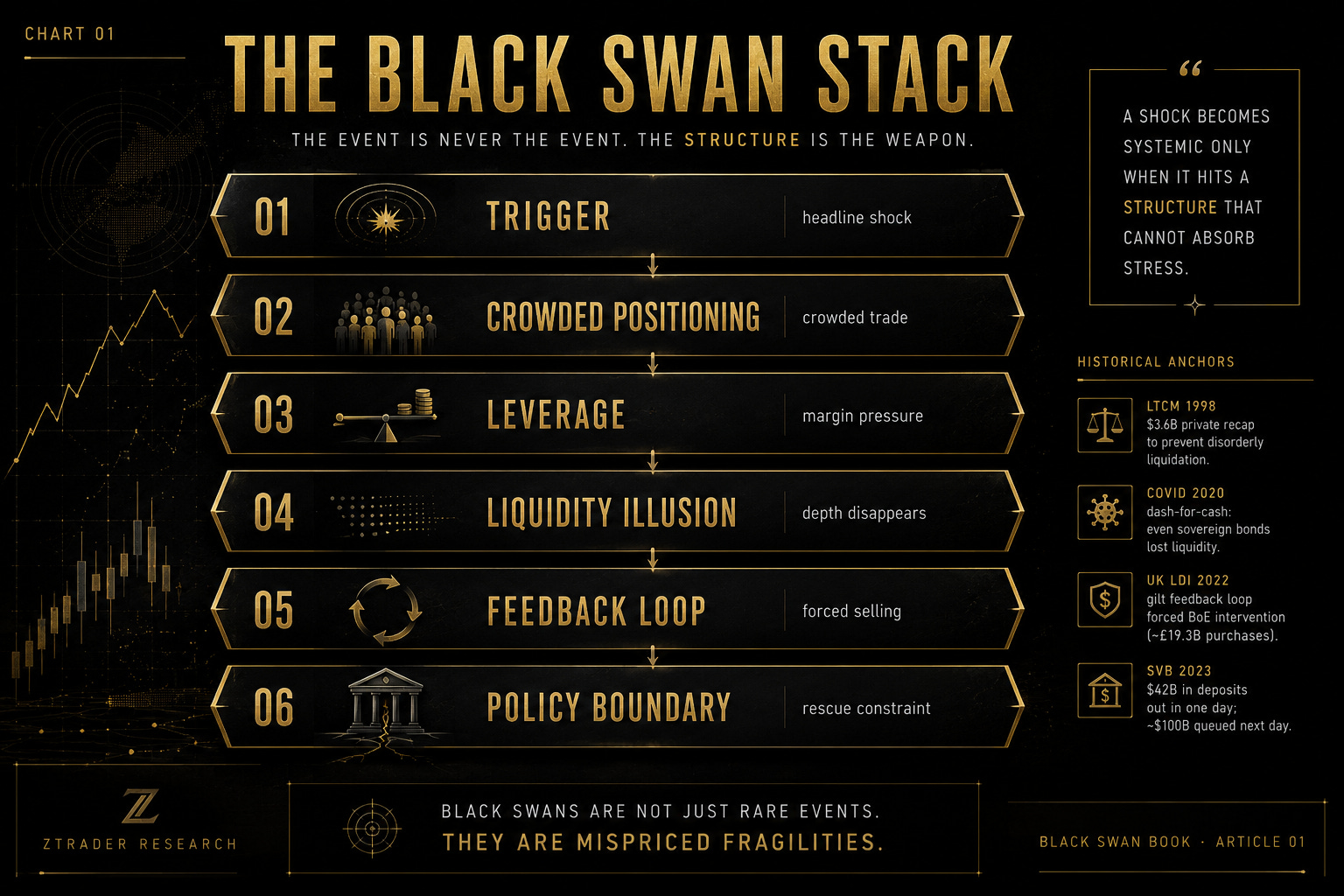

The Black Swan Stack

A financial black swan usually moves through six layers.

The first layer is the trigger.

That is what appears on the screen: war, pandemic, policy error, bank run, inflation surprise, currency shock, credit event, commodity supply break.

The second layer is positioning.

The question is not only whether the news is bad.

The question is who owns the wrong side of the trade.

Crowded long equities/short volatility/carry/long duration.

Crowded Treasury basis/ AI beta and private credit.

A shock against an uncrowded position creates pain.

A shock against a crowded position creates liquidation.

The third layer is leverage.

Leverage decides whether losses are absorbed or transmitted.

Unlevered investors can wait.

Levered investors cannot.

They receive margin calls.

They cut exposure.

They sell what they can, not what they want.

This is why black swan events often become cross-asset events. The original asset may not be the one that gets sold hardest.

The fourth layer is liquidity illusion.

Markets often look liquid until everyone needs the exit at the same time.

Liquidity is not volume.

Liquidity is the ability to sell size without moving the price.

That difference becomes brutal during stress.

A market can trade heavily and still be dysfunctional.

The screen shows prints.

The book shows air.

The fifth layer is the feedback loop.

Price falls.

Margin rises.

Collateral declines.

Hedging demand increases.

Dealers adjust exposure.

Volatility rises.

Risk models cut gross.

More selling follows.

This is the moment when the market stops reacting to the event.

The market becomes the event.

The sixth layer is the policy boundary.

Can the central bank cut?

Can it inject liquidity?

Can it buy assets?

Can it backstop deposits?

Can it stabilize funding without reigniting inflation?

The most dangerous black swans are not always the ones where policymakers do nothing.

They are often the ones where policymakers want to help but are constrained.

Inflation constrains rate cuts.

Politics constrains bailouts.

Currency weakness constrains liquidity.

Fiscal credibility constrains bond-market rescue.

That is where a financial accident becomes a regime shift.

Chart 01 · The Black Swan Stack

The event is never the event. The structure is the weapon. A shock becomes systemic only when it hits positioning, leverage, liquidity, feedback loops, and policy constraints.

A Simple Rule

The first job of black swan research is not prediction.

It is mapping.

Prediction asks for the exact event.

Mapping asks where the system cannot absorb stress.

That means watching the distance between market pricing and structural vulnerability.

When volatility is low, credit spreads are tight, funding stress is quiet, and liquidity looks normal, the market is not automatically safe.

It may simply be calm.

Calm is not the same as resilient.

Resilience means the system can absorb a shock without forced selling.

Calm only means the shock has not arrived yet.

This distinction matters because markets often look best near the point where fragility is most ignored.

Low volatility encourages leverage.

Tight credit spreads encourage yield chasing.

Stable FX encourages carry trades.

Liquid markets encourage bigger position size.

Policy confidence encourages investors to underprice tail risk.

The system becomes more fragile because nothing bad has happened recently.

That is the trap.

The absence of stress becomes the reason to add stress.