AUSTRALIA'S BANKS ARE THE REAL AUD TRADE NOW

The Aussie fell 3.9% in a month. The positioning data says the currency isn't the trade — the mortgage book is.

By Dorian

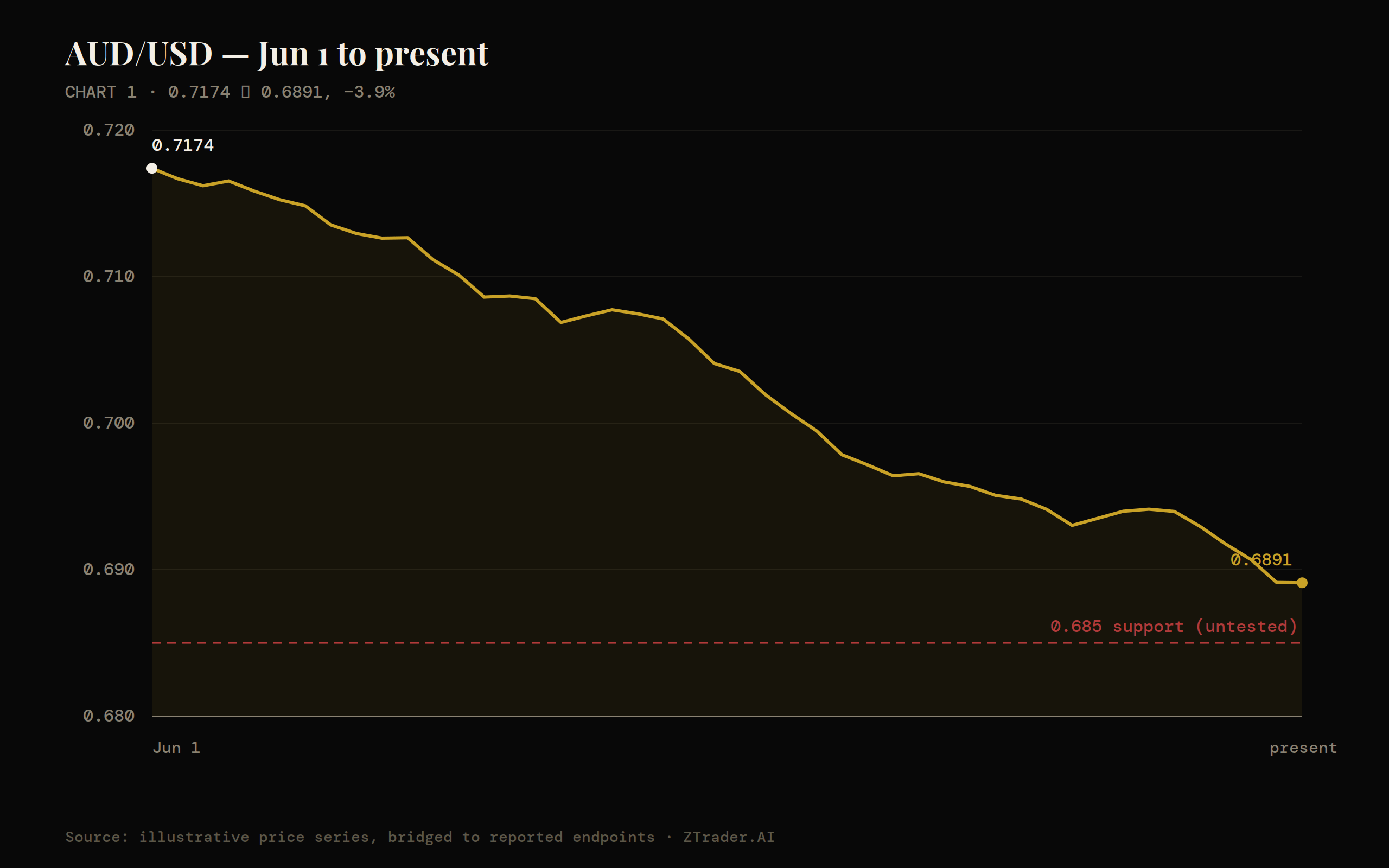

[CHART 1 — AUD/USD, June 1 – present, with 0.685 support level marked]

On June 1, AUD/USD traded at 0.7174. By the last week of June it was at 0.6891. A 3.9% move in a G10 pair over four weeks is not noise — it's a repricing. But look at who's doing the repricing, and the story stops being about the currency at all.

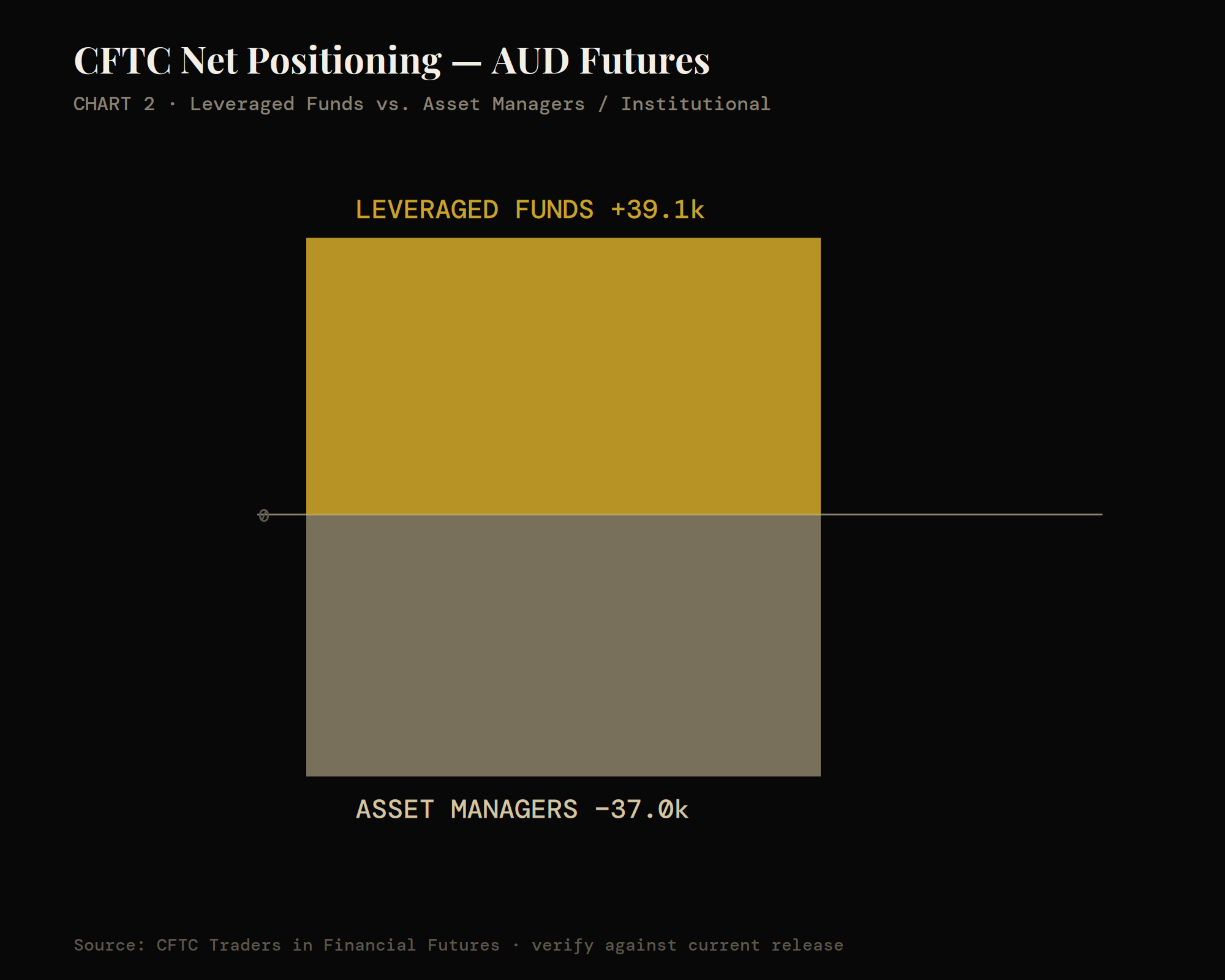

CFTC futures data shows leveraged funds still net long AUD by roughly 39.1k contracts. That's fast money — CTAs, macro funds, the crowd that trades trend and carry.

At the same time, asset managers and other institutional accounts are net short by about 37.0k contracts.

Two sophisticated pools of capital, looking at the same chart, taking opposite sides.

[CHART 2 — CFTC net positioning, Leveraged Funds vs Asset Managers, AUD futures]

That split alone would be worth a paragraph. What makes it a thesis is the third data point: equity long-short funds have built an estimated A$11bn in short exposure against Australia's big four banks — Commonwealth, Westpac, NAB, ANZ. That's not a currency bet.

That's a bet on what's sitting on those banks' balance sheets.

Put the three together and a shape emerges.

The FX crowd is still buying the carry trade — rate differential, commodity beta, muscle memory. The institutional book is already de-risking the currency. And the equity funds, the ones whose job is to know a balance sheet before anyone else does, are shorting the exact institutions that would take the first hit if Australian housing credit turns.

And That's precisely the misread.

AUD/USD below 0.69 looks like a rate story or a China-proxy story, and header writers will file it that way. The positioning underneath says otherwise: it's a preview of stress in the mortgage-heavy core of the Australian financial system, and the currency is just the instrument that moves first because it's the most liquid.

So Here's the mechanism.

Australia's big four banks carry mortgage books that are unusually concentrated relative to GDP even by developed-market standards — housing credit sits close to 130-140% of household income in aggregate, and the banks fund a large share of that book through wholesale markets rather than pure deposits.

When offshore funding costs rise or currency volatility increases, the marginal cost of rolling that wholesale funding rises with it. That's the first-order channel: AUD weakness and funding stress aren't separate stories, they're the same story told from two desks.

Australia has been here before, structurally if not literally.

In 2008, the same wholesale-funding dependency forced the government to guarantee bank liabilities within weeks of Lehman, not because the mortgage book was bad but because the funding model couldn't survive a global freeze.

In 2011, during the European sovereign crisis, the same mechanism showed up again — AUD sold off on risk-off flows well before any Australian-specific credit event, because offshore investors treat AUD as the most liquid proxy for "risk that isn't in this room." The pattern is consistent: Australia's financial system doesn't generate its own crises very often. It imports funding stress through the currency and transmits it into the banks. That's precisely the sequence the current positioning data is describing before it happens rather than after.

Subscribe to unlock for the remaining market insight: